Trump’s big beautiful bill is negligible in terms of economic impulse. Accompanied by 10-12% average tariffs the whole policy change is contractionary. Inflation can undershoot expectations due to continuing disinflation in shelter and services. Earnings and employment should suffer more.

Despite all the bill headlines, economists haven’t altered their fiscal forecasts since Trump started leading the polls in summer 2024. Apart from frontloaded corporate investment tax deduction, aggregate impulse of the bill is absent.

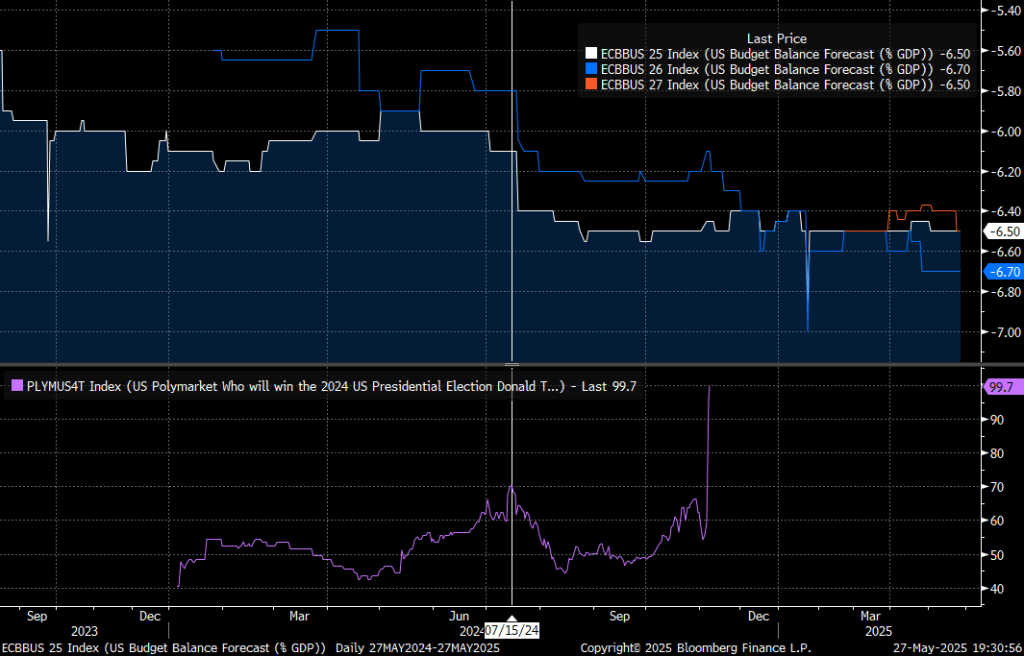

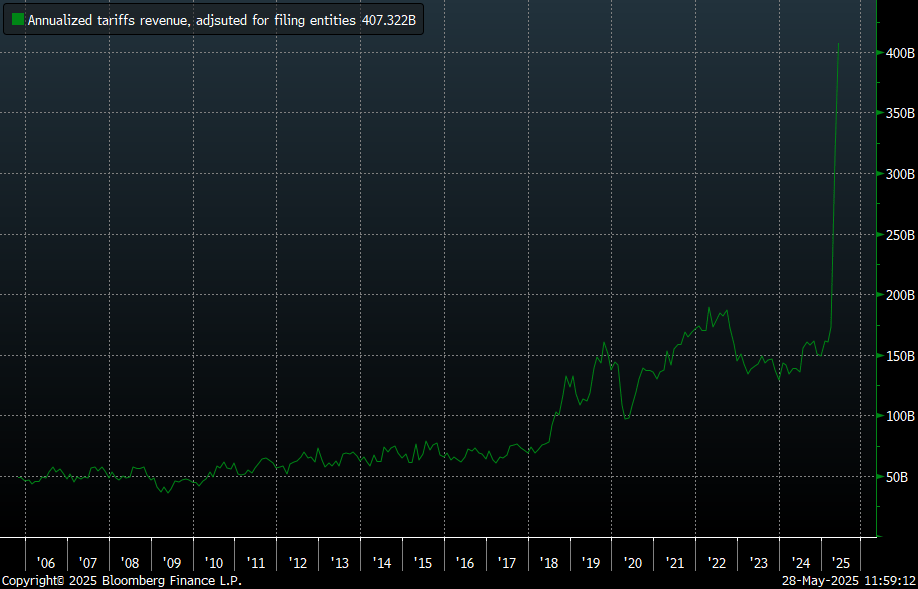

Meanwhile April tariffs revenue (or cost to importers) was around $22bn. Annualized and adjusted for number of companies that file monthly (2/3 of total) it is around $400bn: 10% of imports or 1.5% of GDP. This new source of fiscal tightening is effectively reducing government deficit to 5.0-5.5% from 6.5% projected.

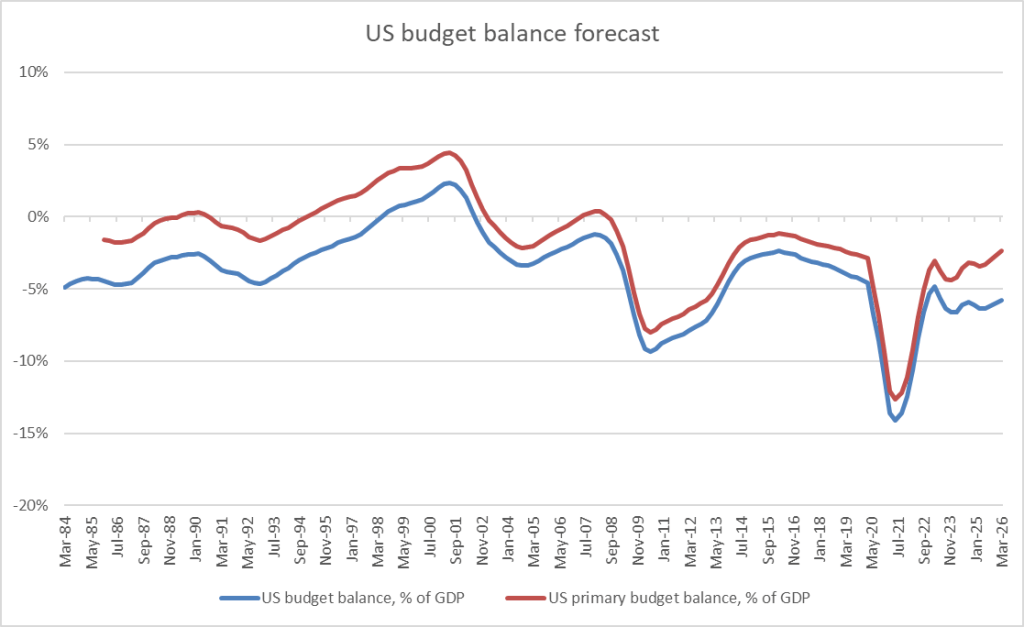

At the same time, interest expense is the quickest growing government cost, contributing 3-3.5% of GDP to the deficit.

Netting both tariffs and interest, primary deficit is expected to decline to around 2.5% in a year, assuming effective 10% tariffs on all imports. From ~3.5% at the moment.

Inflation can undershoot elevated tariff-caused expectations, as wages are slowing, services inflation is normalizing and housing market is rolling over, negatively affecting shelter part of the CPI. Initial reciprocal tariffs was a surprise. However, once negotiations started, expectations started to moderate. FED, meanwhile, is in the wait and see mode.

Actual shelter inflation is half of official numbers, which contributes 1.4pp to official 2.3% yoy CPI. Adjusting for the lag, headline CPI is around 1.5% at the moment.

Median services inflation is moderating. Companies are adjusting prices slower than in the last 3 years. But still more than before Covid.

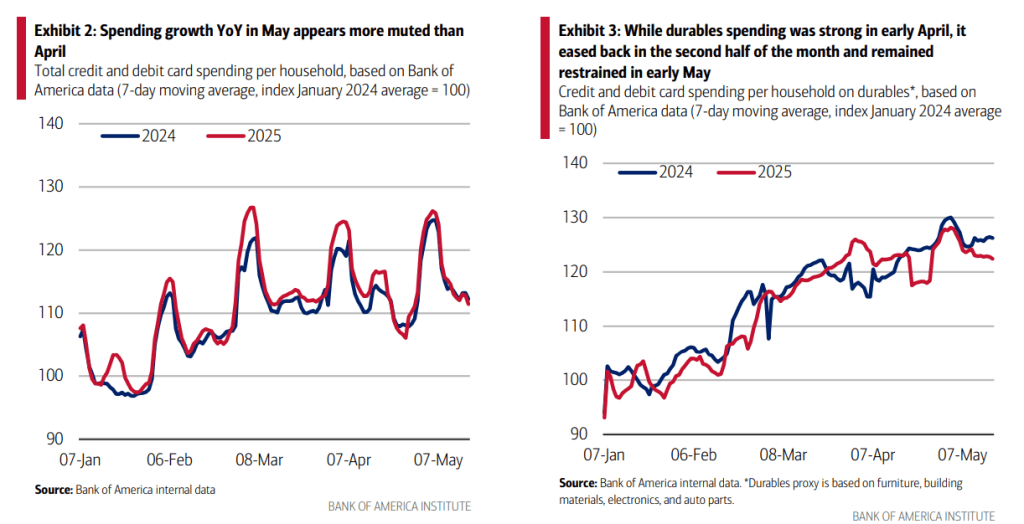

Moving to growth, consumer spending still remains robust but is driven by tariffs front running. Car sales are already expected to decline in May from strong March and April figures.

Credit card spending is slowing after the initial tariffs surge.

Demand weakness is mentioned more often during corporate earning calls.

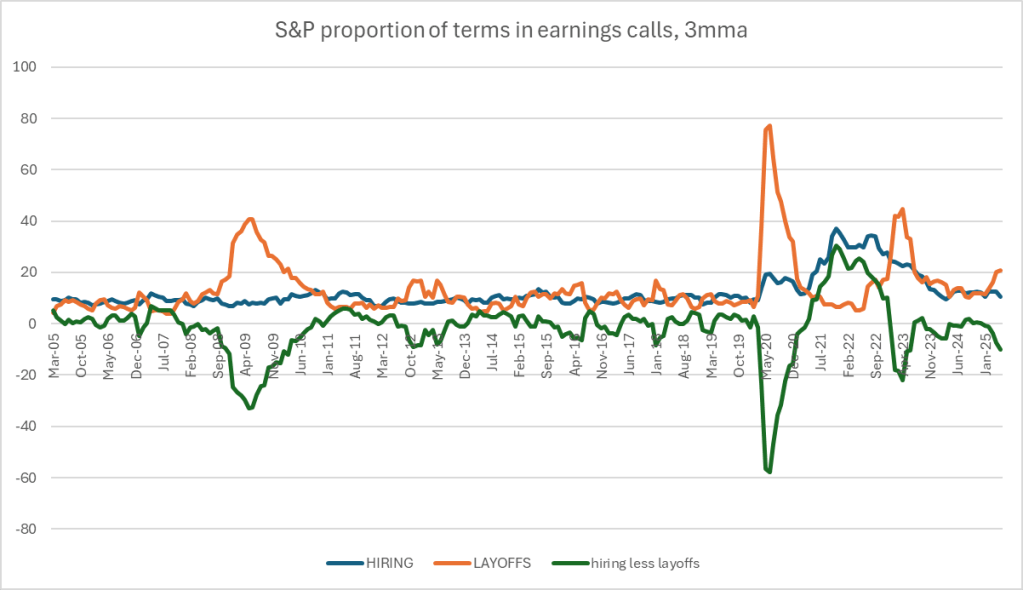

This is also translating into weaker labor market. S&P employment sentiment dropped in April and May, probably still affected by DOGE headlines. But sharp tariffs announcement didn’t help either.

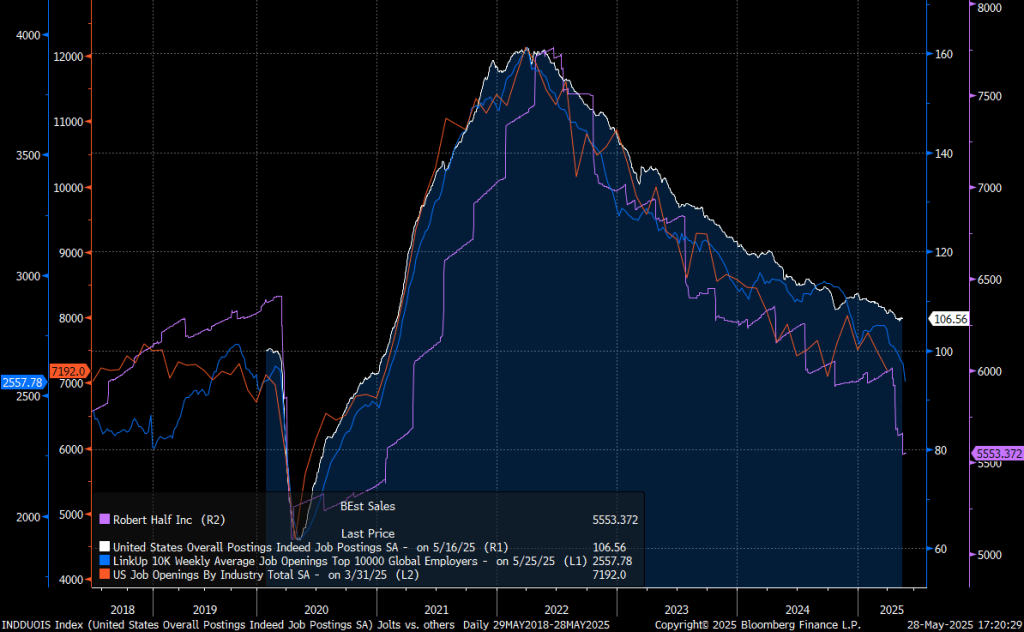

Job postings continue to deteriorate and haven’t improved since trade talks started.

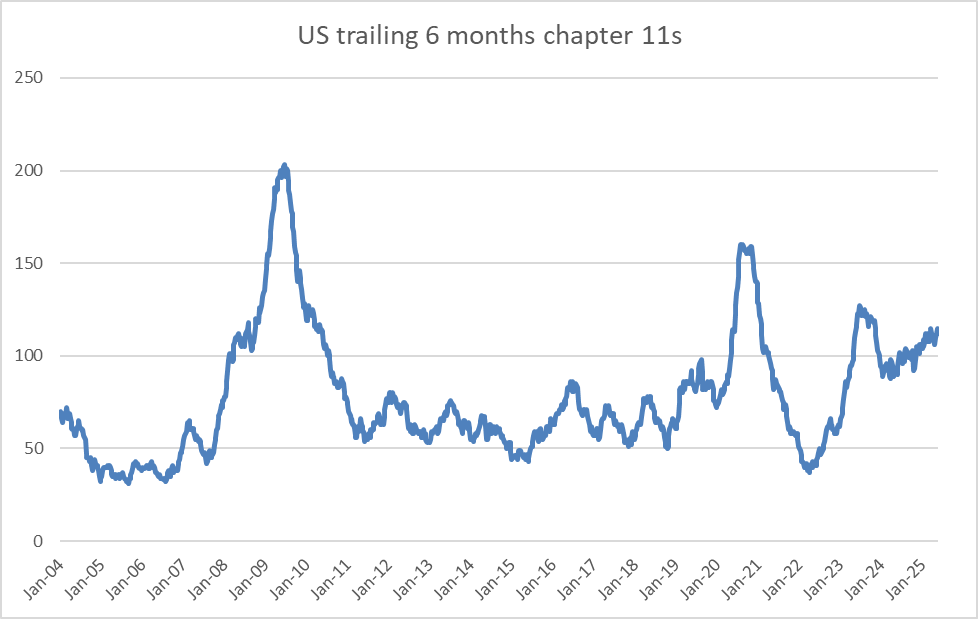

Chapter 11 filings are slowly trending higher. Putting extra pressure on unemployment.

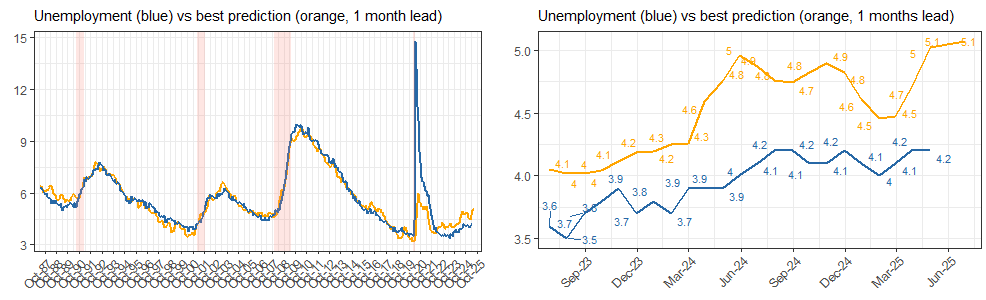

Unemployment expectations are rising again after a dip in Q1.

These all adds to the political risks that US assets are facing. To my mind, it creates attractive opportunities in Fed easing expectations through SOFR calls. US equities face more downside, particularly after the “liberation day” bounce. Low price long term bonds have interesting risk/reward profile, as they should still work in a recessionary scenario.

Leave a comment