Trying to make sense of economic shifts and asset prices

-

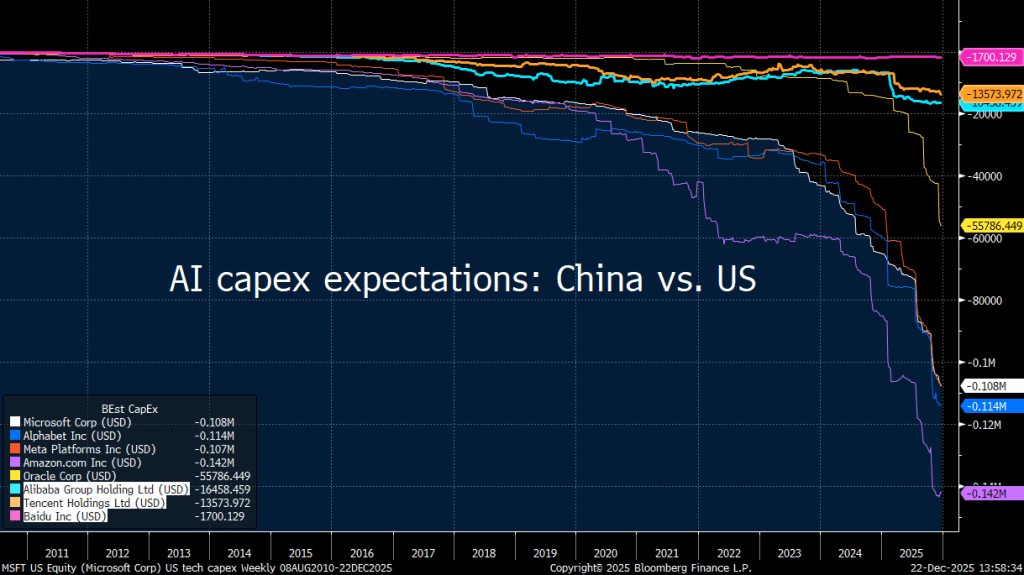

2026 predictions (and 2025 review)

First, 2025 review. Recession didn’t happen. At least looking at financial markets. Common theme by the end of the year formed as: “there’s not enough exuberance about AI”. More detailed view below. And yes, risk of US recession is still high.

-

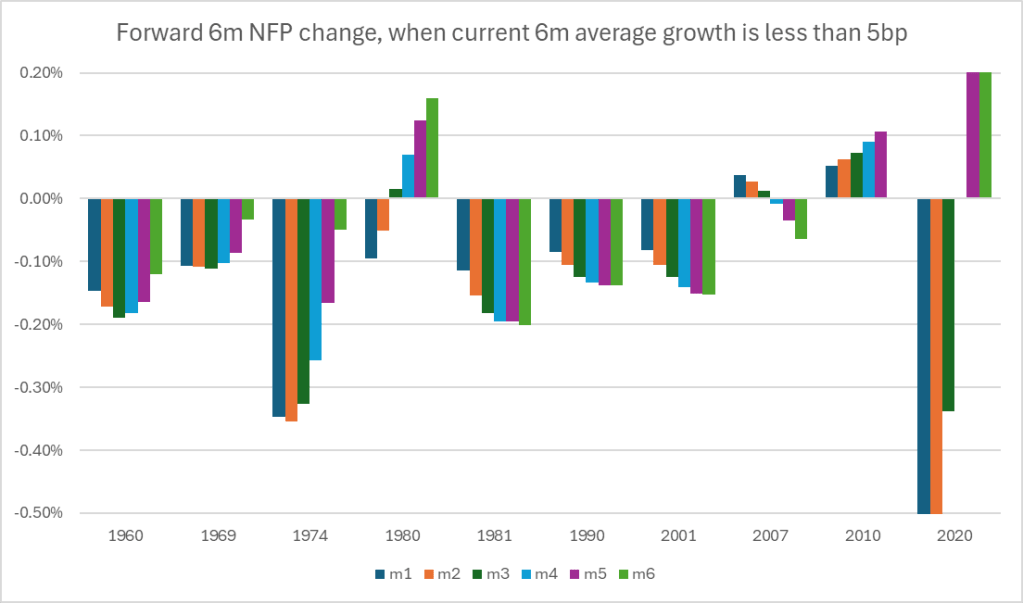

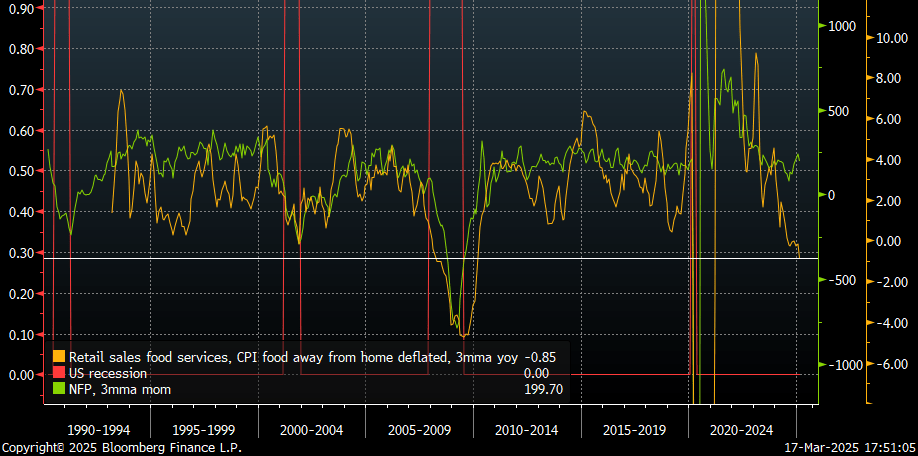

Recession in the US

US is in recession, based on the last 2 employment reports and labor benchmark revisions. Most probably NFP was negative during several months in 2024 already. And it’s hardly positive right now. Asset prices, AI capex, and consumers willingness to reduce savings rate maintained aggregate growth of the economy. If current labor weakness spirals, there’s…

-

First shocking NFP print in a while: US equities mask growing risks

Inflation continues to miss expectations and labor market apparently has been weak since April, judging by the large NFP revisions. Tariffs prove to be a catalyst for a slowdown in US economy, but not in US (AI) stocks yet.

-

Big Beautiful Bill, Tariffs, Inflation, US Consumer — more downside in US stocks

Trump’s big beautiful bill is negligible in terms of economic impulse. Accompanied by 10-12% average tariffs the whole policy change is contractionary. Inflation can undershoot expectations due to continuing disinflation in shelter and services. Earnings and employment should suffer more.

-

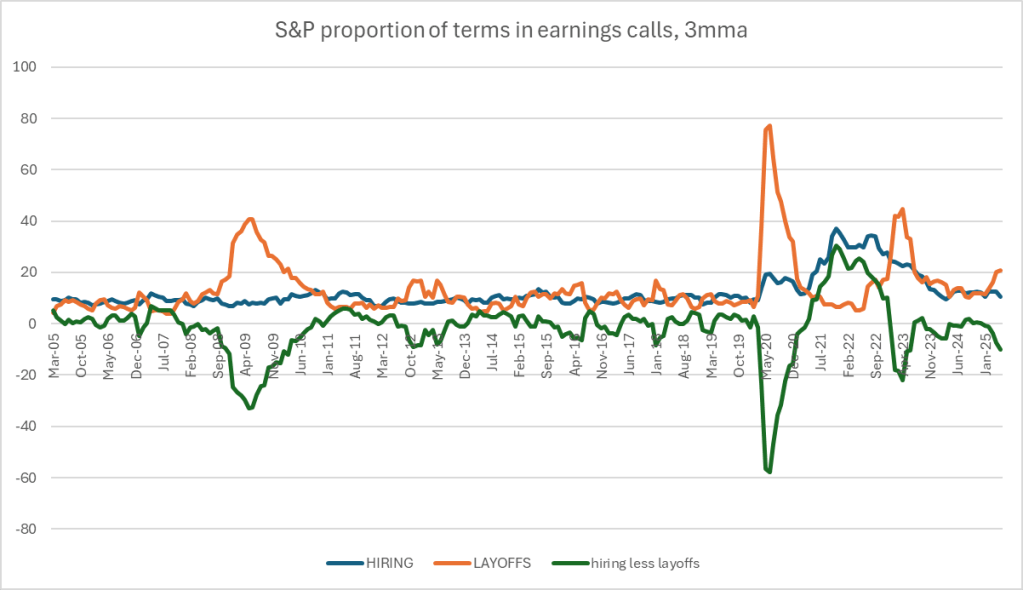

US economic weakness spreading into consumers

US consumer activity is rolling over, following the first layoffs and poor stock market performance. Employment has deteriorated and is expected to increase further. And policy put might be lower than what people wished for. FED might be forced to stay too restrictive given unfavorable core CPI and PPI mixes.

-

US economic momentum softens, new data rolls off quickly

Newly released economic data out of US is rolling over quickly. At first glance, Trump tariff policy and Doge employment actions are raising uncertainty and reducing activity. In fact, economy has already been showing topping signs for a while. Lack of layoffs and aggregate corporate earnings were key pillars of the current cycle. But this…

-

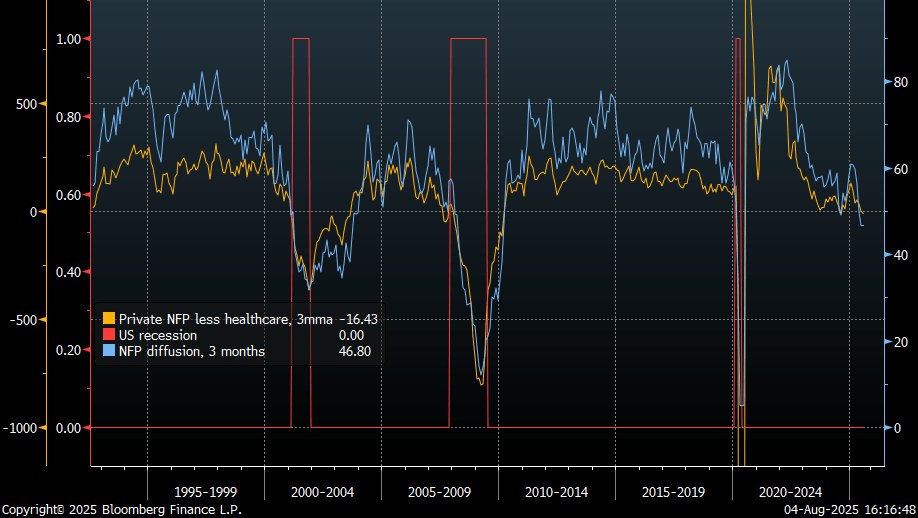

US employment market continues to soften

Recent labor market data shows a significant revision, with household survey employment up 2.2 million, revealing that the 2024 employment count was substantially underestimated. A number of other various indicators are showing labor market is softening further and raises questions about the last unemployment rate.

-

Stronger US labor numbers in December, but risks skewed to the downside

The US labor market showed improvement in December with increased non-farm payrolls and lower unemployment. However, mixed labor indicators suggest uncertainty remains, as actual hiring contrasts with improved corporate expectations. Risks of higher unemployment rate persist, complicating future labor trends.

-

Trade idea: Long SOFR March 2025 call spreads

Since I believe US unemployment should be a bit higher in December and January, given difficulty of finding a new job and declining job ads, I got into some SOFR March call spreads before December nonfarm payrolls report. I find odds of more cuts being price in during the next two Fed meetings attractive.

-

2025 predictions: US equities and yields down, China outperforms, credit risk jumps

Risk of US recession is increasing: tariffs reduce aggregate demand, housing market is deflating, business capex set to decline after IRA and AI boost, personal consumption will slowdown due to higher unemployment rate and weaker wealth effect, fiscal impulse disappears