US labor market momentum improved strongly in December after higher than expected non-farm payrolls and lower unemployment. Retail trade seasonal increase in employment was registered in December due to the calendar effects. And firms probably cleared hiring backlogs after the election results. Both will be a drag in the next reports.

Is labor market reversing and accelerating again? Doubtfully. Many labor indicators are mixed. Some, which are mostly based on corporate expectations, are improving. Others, more actual, are stable or weaker. Unemployment run rate is around 4.5% at the moment, based on various regressions. Risks of the higher unemployment rate remain.

To begin, actual flow of people not in labor force to employment is declining further. But people remain employed longer compared to previous labor softening cycles, judging by employed-to-employed flows.

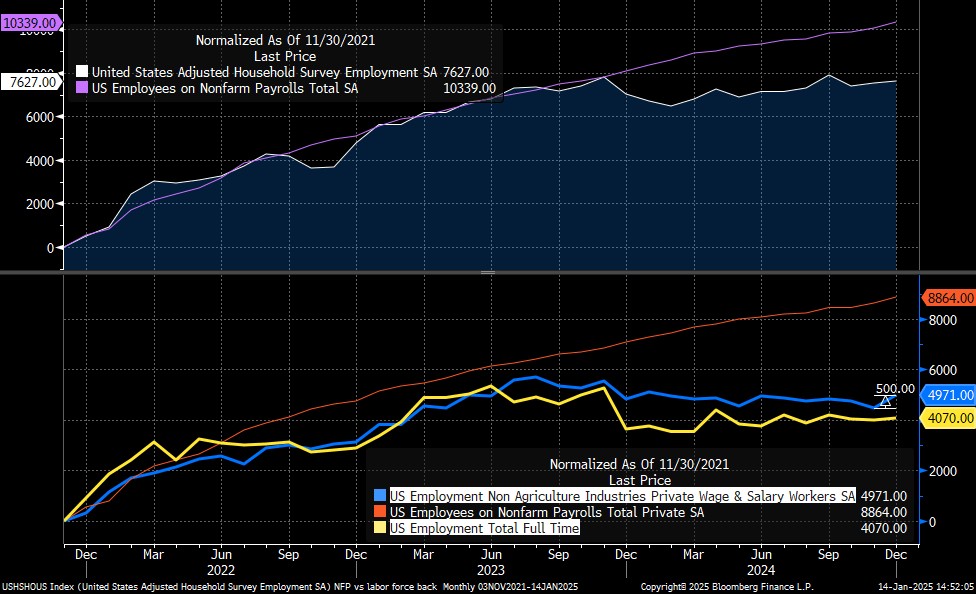

Household survey registered a strong increase in private employment in December: +500k of private non agriculture jobs. Nonetheless, full time employment has barely moved. Household survey is further diverging from NFP.

Both NFP and household surveys was also significantly affected by retail sales jobs. NFP retail trade category increased by 49k m/m. Household survey “sales and related” jumped by more than 500k on a seasonally adjusted basis. Some of that could be given back in the next reports.

Moving to alternative indicators, University of Michigan consumer expectations of 1-year unemployment deteriorated significantly in January. Current level, especially its 6-month moving average, isn’t always indicative of recessions, but it’s also much worse than in January 2017, the first Trump’s January.

While NFIB small businesses hiring plans jump, similarly to other NFIB expectations sub-components. This is similar to the first Trump term as well.

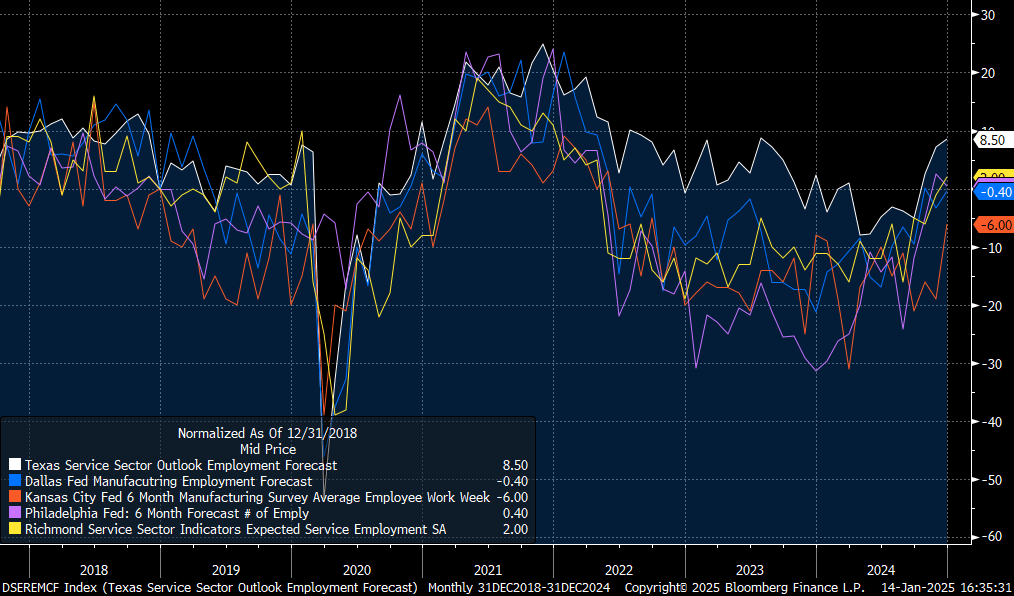

Hiring expectations are also stronger in a number of other regional Fed surveys.

But actual change in employment per firm, according to NFIB, is down to a new cycle low.

And a lower number of firms is raising wages now, which usually happens in a weaker labor market, with unemployment closer to 4.5% (based on a simple regression with pre-Covid sample).

We’ll see whether expectations will affect current behavior, or just mislead about the reacceleration narrative. Risks of higher unemployment rate stay high.

Leave a comment