Trump trade so far is diverging from 2016 analogy. At the moment most markets see much smaller incremental policy change compared to 2016. On top of that, rates stay restrictive enough to slow the economy further: demand, employment, margins, inflation – are all softening.

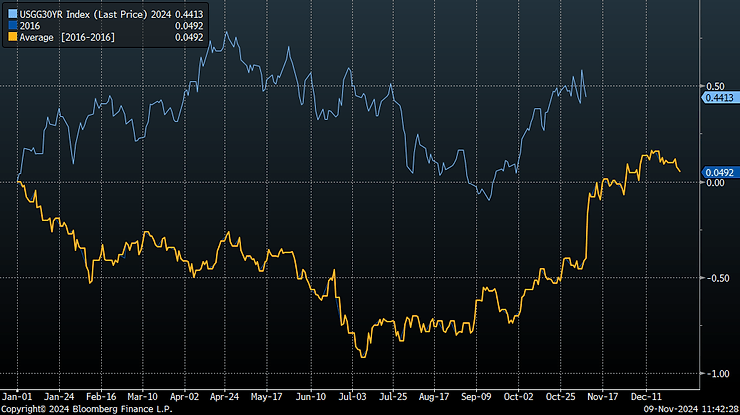

Bonds aren’t selling off post elections, despite large intraday volatility on the election date. 30-year yields are basically flat in the last 2 weeks.

Dollar strengthens less than in 2016 too (percent change ytd).

So are inflation swaps (actual value).

(more…)