Trump’s big beautiful bill is negligible in terms of economic impulse. Accompanied by 10-12% average tariffs the whole policy change is contractionary. Inflation can undershoot expectations due to continuing disinflation in shelter and services. Earnings and employment should suffer more.

Despite all the bill headlines, economists haven’t altered their fiscal forecasts since Trump started leading the polls in summer 2024. Apart from frontloaded corporate investment tax deduction, aggregate impulse of the bill is absent.

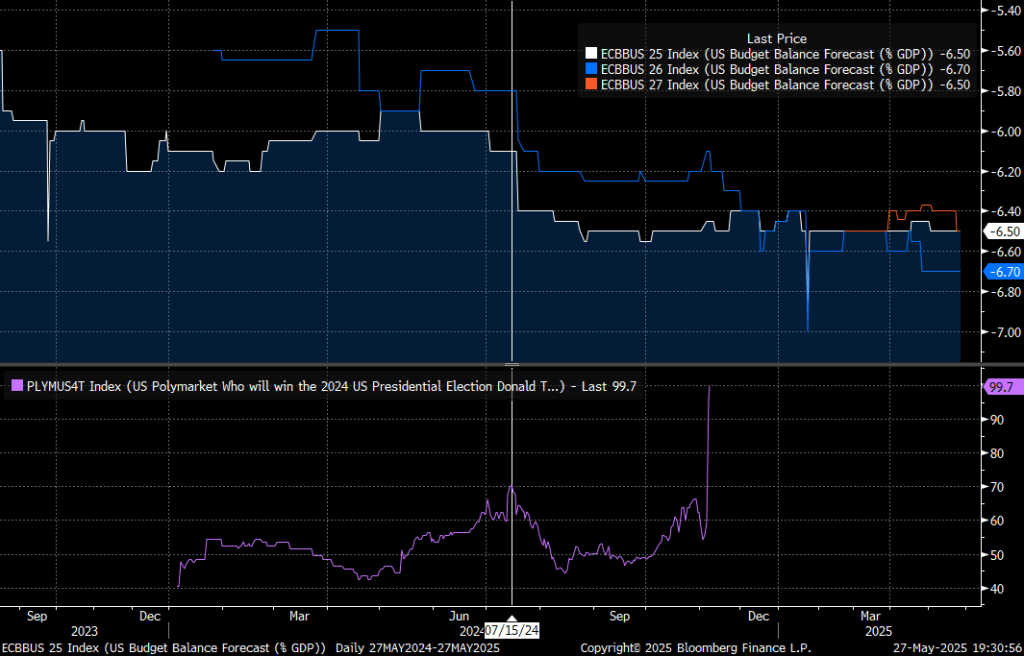

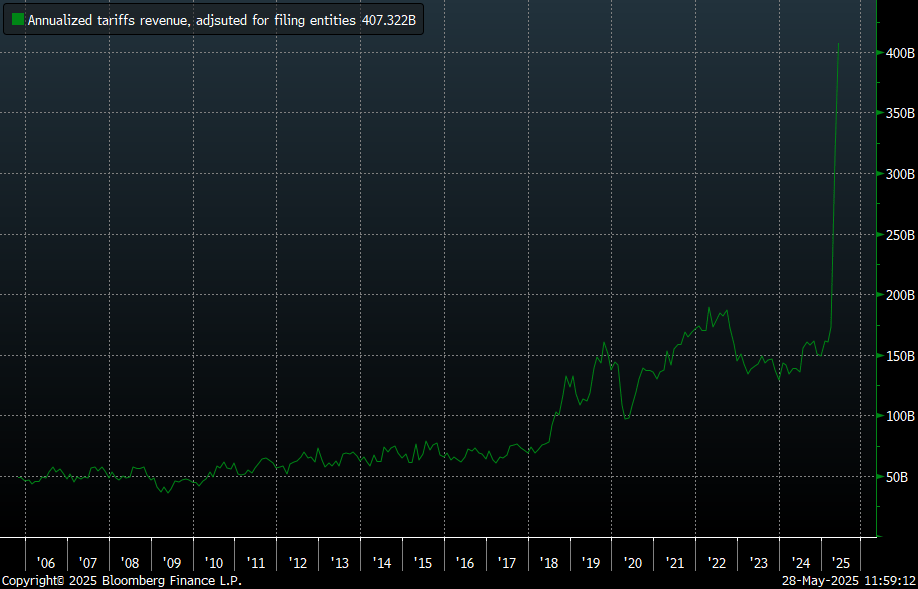

Meanwhile April tariffs revenue (or cost to importers) was around $22bn. Annualized and adjusted for number of companies that file monthly (2/3 of total) it is around $400bn: 10% of imports or 1.5% of GDP. This new source of fiscal tightening is effectively reducing government deficit to 5.0-5.5% from 6.5% projected.

At the same time, interest expense is the quickest growing government cost, contributing 3-3.5% of GDP to the deficit.

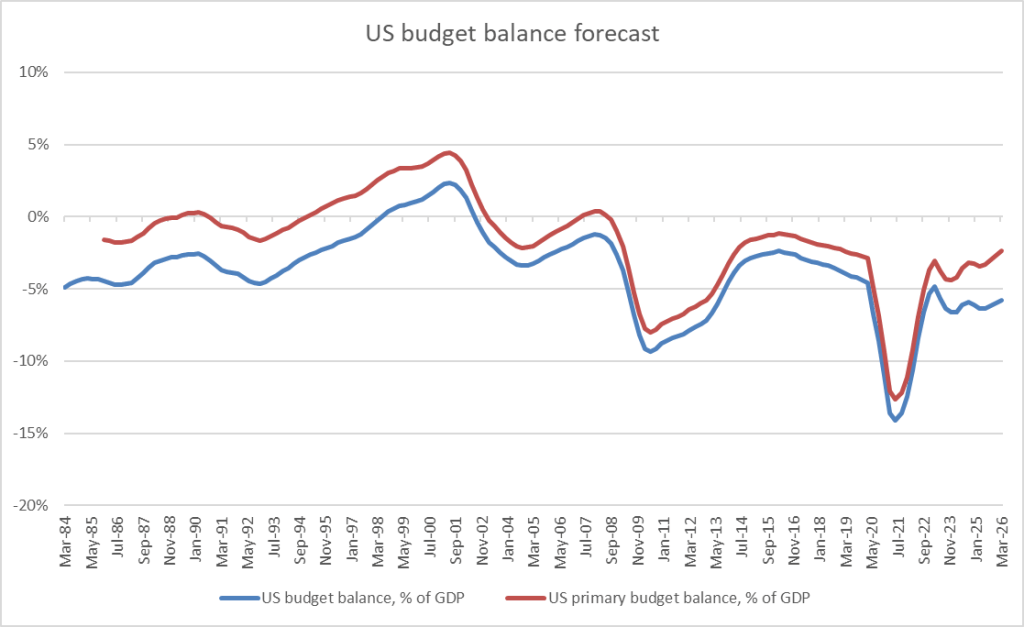

Netting both tariffs and interest, primary deficit is expected to decline to around 2.5% in a year, assuming effective 10% tariffs on all imports. From ~3.5% at the moment.

Inflation can undershoot elevated tariff-caused expectations, as wages are slowing, services inflation is normalizing and housing market is rolling over, negatively affecting shelter part of the CPI. Initial reciprocal tariffs was a surprise. However, once negotiations started, expectations started to moderate. FED, meanwhile, is in the wait and see mode.

Actual shelter inflation is half of official numbers, which contributes 1.4pp to official 2.3% yoy CPI. Adjusting for the lag, headline CPI is around 1.5% at the moment.

Median services inflation is moderating. Companies are adjusting prices slower than in the last 3 years. But still more than before Covid.

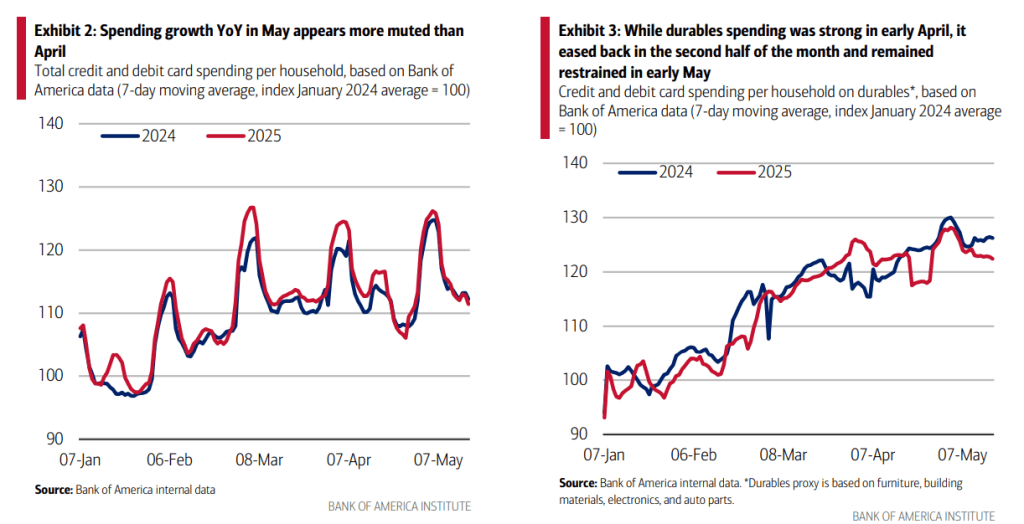

Moving to growth, consumer spending still remains robust but is driven by tariffs front running. Car sales are already expected to decline in May from strong March and April figures.

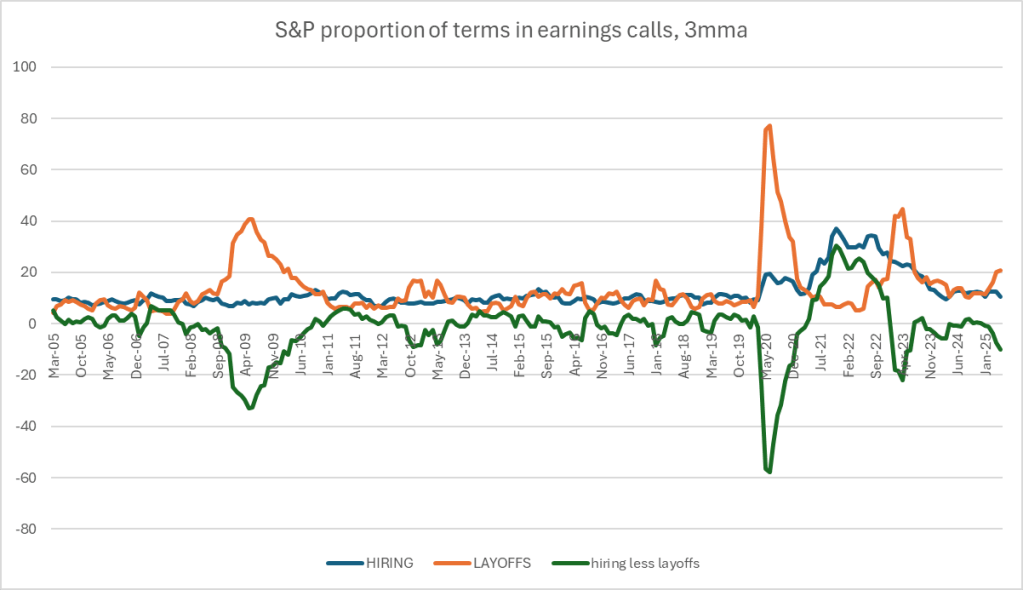

Demand weakness is mentioned more often during corporate earning calls.

This is also translating into weaker labor market. S&P employment sentiment dropped in April and May, probably still affected by DOGE headlines. But sharp tariffs announcement didn’t help either.

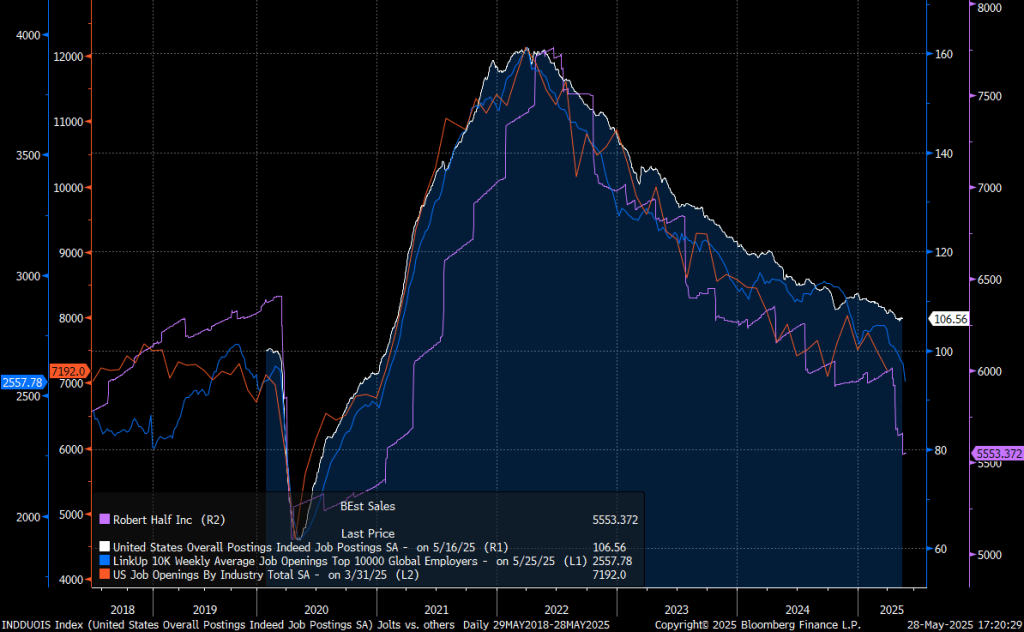

Job postings continue to deteriorate and haven’t improved since trade talks started.

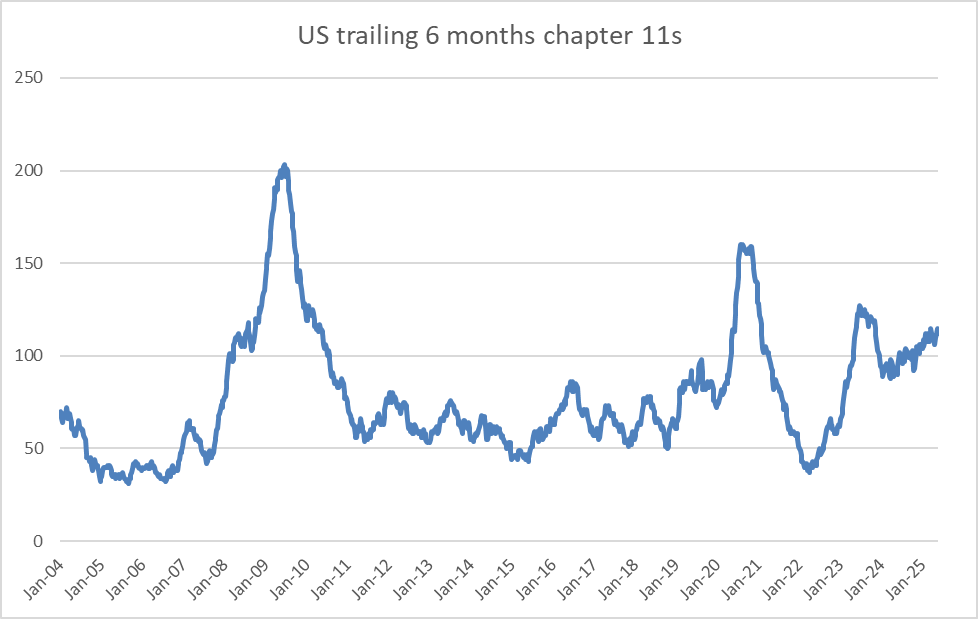

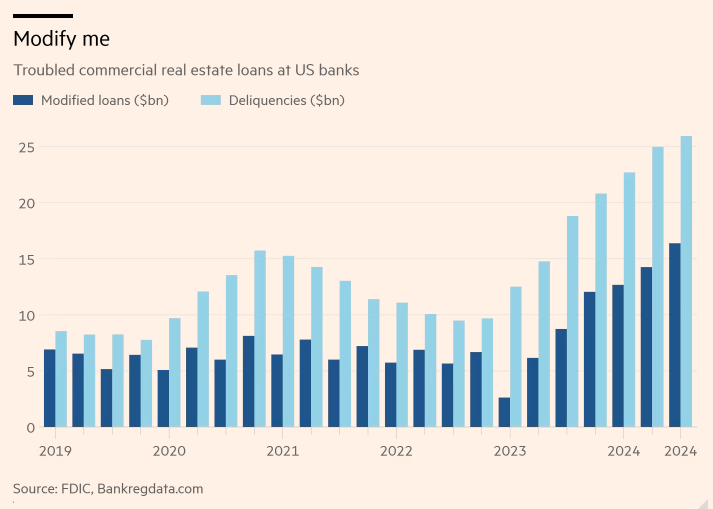

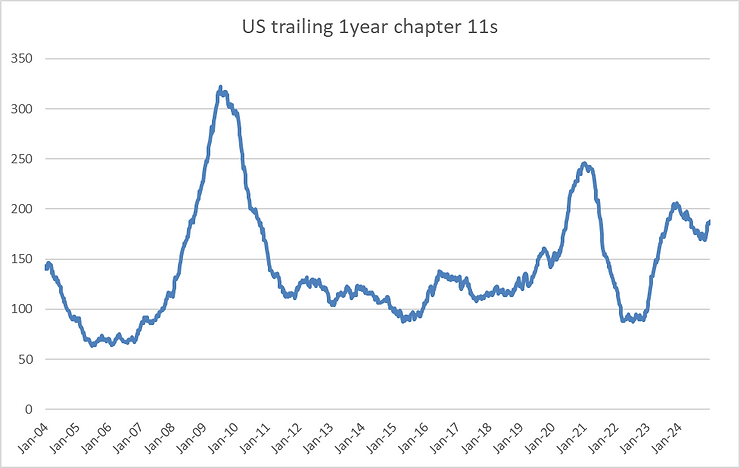

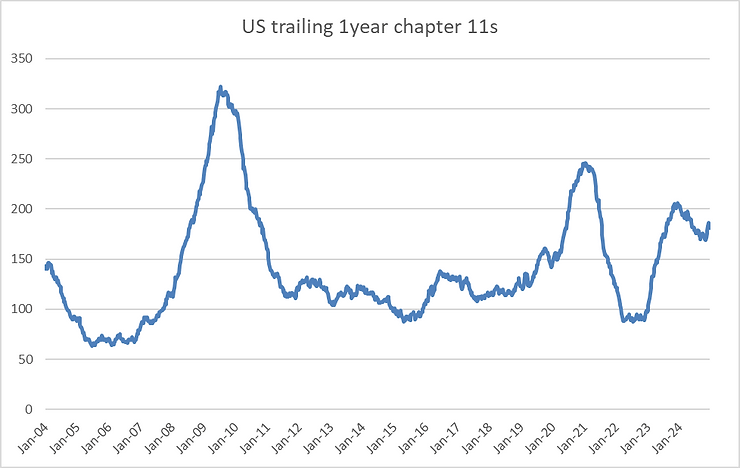

Chapter 11 filings are slowly trending higher. Putting extra pressure on unemployment.

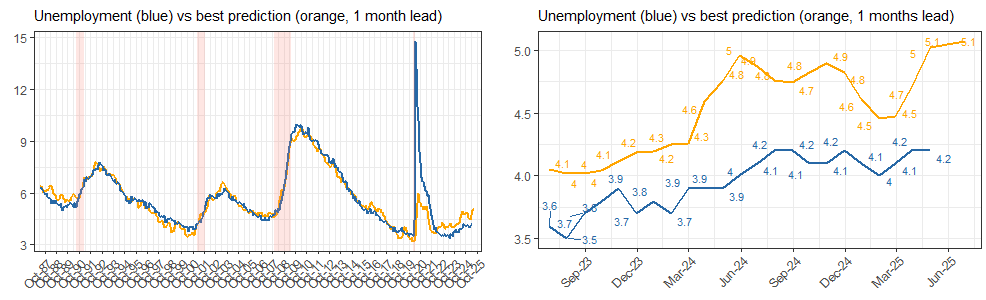

Unemployment expectations are rising again after a dip in Q1.

These all adds to the political risks that US assets are facing. To my mind, it creates attractive opportunities in Fed easing expectations through SOFR calls. US equities face more downside, particularly after the “liberation day” bounce. Low price long term bonds have interesting risk/reward profile, as they should still work in a recessionary scenario.

Risk of US recession is increasing: tariffs reduce aggregate demand, housing market is deflating, business capex set to decline after IRA and AI boost, personal consumption will slowdown due to higher unemployment rate and weaker wealth effect, fiscal impulse disappears. S&P and risk assets fall, but not because of higher rates. As Fed turns dovish, 2 year yields rally.

Tariffs. US GDP will drop due to higher costs and lower demand, offset by corporate tax cuts, and prices inside the US will jump again. But it will help with deflation outside of the US.

Estimates of GDP decline vary across economists, but conclusion is similar. US will require substantial fiscal stimulus to diminish negative effect from tariffs.

Moreover, the first round of tariffs had negative cumulative effect on US employment mostly due to rising import costs and foreign retaliation, according to Fed.

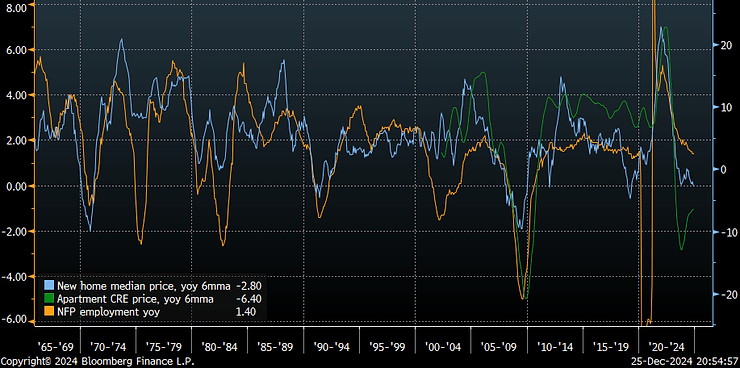

Housing market. Number of houses for sale is rising quickly at moment, even when normalized by actual number of new homes sold. This kind of inventory accumulation was associated with prior recessions and falls in general employment.

As a result deflation in housing is spreading. Implications for general inflation are also negative.

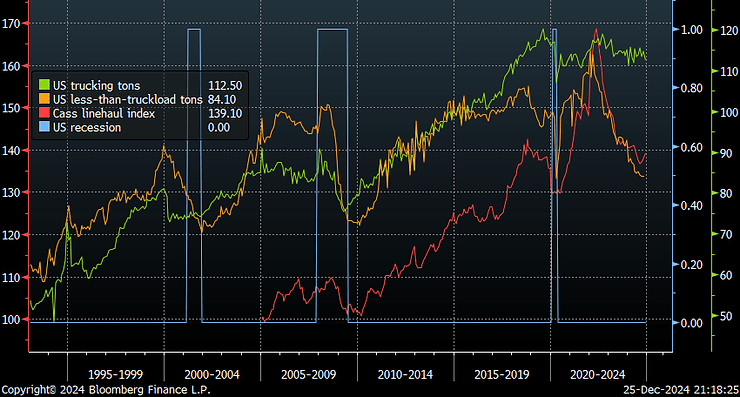

Business capex. Nonresidential construction planning (AI data centers, offices, warehouses, retail etc) is slowing down.

US trucking remains in recession, as commercial capex ex AI has been slowing down since early 2023.

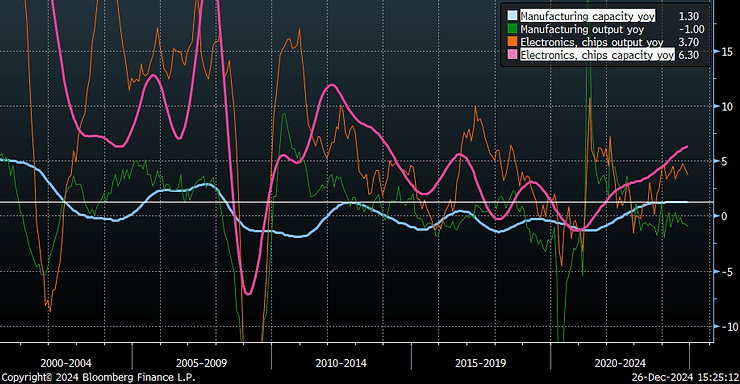

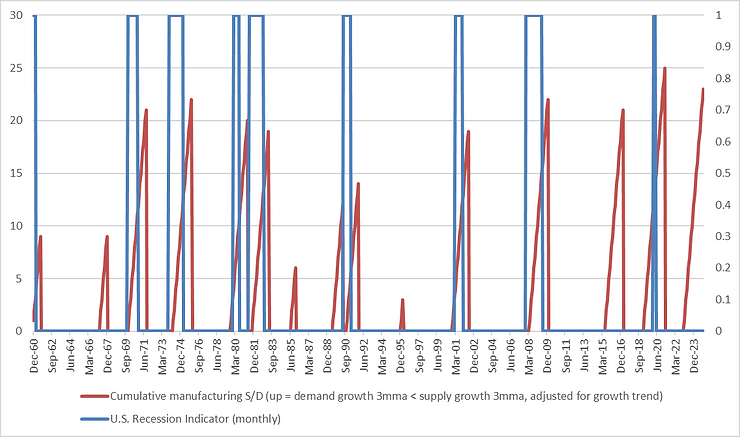

US manufacturing capacity is growing at 1.5% yoy, the fastest pace since 2012. Electronics (including semis) capacity is growing at much faster 6.3% yoy. But overall manufacturing output is down 1% yoy and has been lagging capacity expansion for 2 years now.

The lack of manufacturing output growth leads to declines in capacity utilization and higher unemployment historically. This is usually followed by long business capex slowdowns.

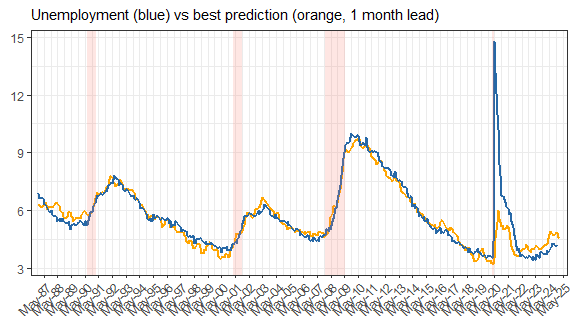

Unemployment. Employment intention proxies remain weak. At the moment there’s no boost expected from any of the Trump policies, according to soft indicators.

Consumer and small businesses surveys are consistent with unemployment of around 4.5-4.6% at the moment.

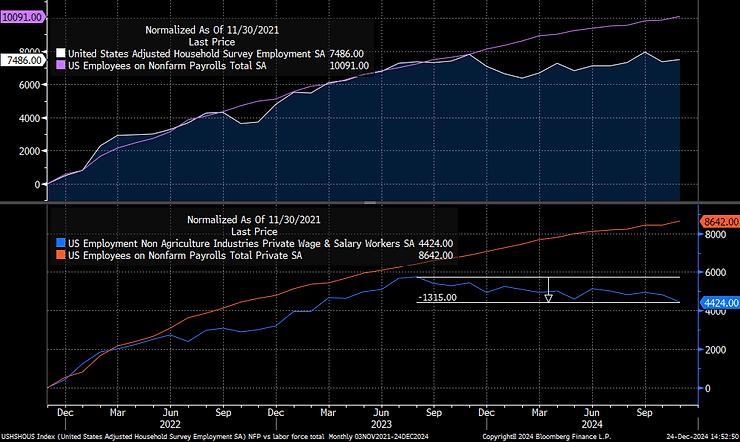

Private employment lost 1.3mn of jobs in the last year and a half, according to household survey. Total private household employment is up 4.4mn in the last 3 years. That compares to 10mn of private and public jobs added, according to NFP survey.

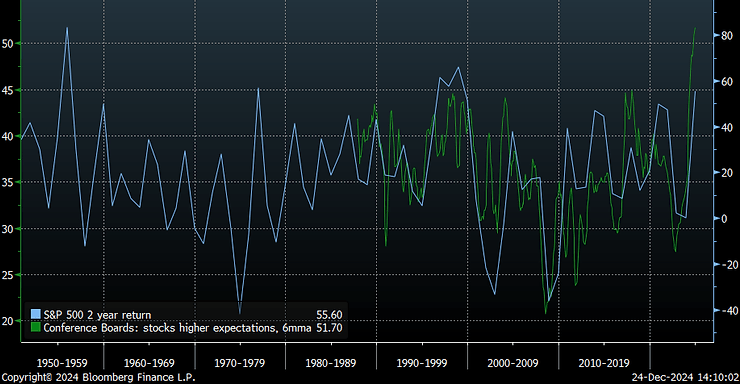

Wealth effect. S&P returned roughly 26% in 2024, one of the largest amounts in the last 30 years. Average S&P return during this period was 8.5%.

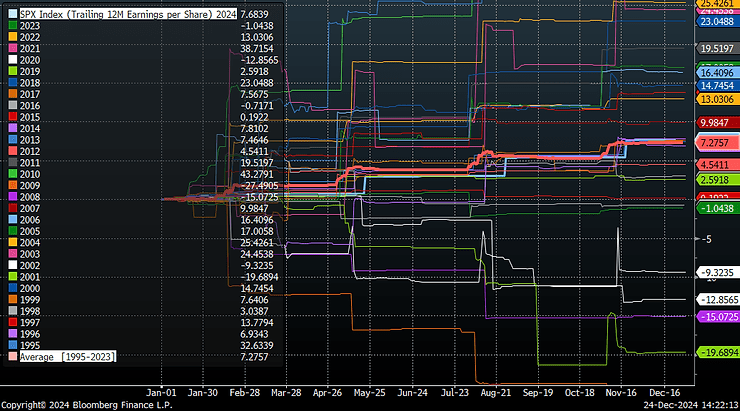

At the same time, trailing 12 months EPS is up 7.7% this year, marginally above average 7.3%.

The index jumped 55% over the last 2 years – one of the best runs ever. That unsurprisingly entrenched into most recent consumer expectations and boosted actual net worth.

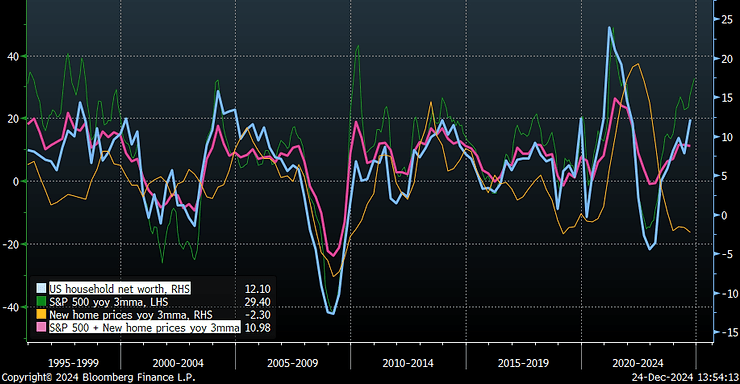

US households net worth is rising at around 12% yoy at the moment. This is roughly in line with an average of S&P returns and new home prices. While housing is already peaking and prices are declining, stock market (and Bitcoin) is maintaining strong wealth effect for households. Unfortunately, the current ramp up in net worth is not driven by owning companies, that generate excess business returns but to a large extent is a result of equity multiples expansion.

Fiscal impulse. Economists expects US budget deficit to remain at 6.5% over 2024-2026, and government debt to add 4.5% of GDP during the period. Fiscal impulse will again recede to zero in this scenario after roughly $1.2tn of incremental impulse since 2022.

US GDP significantly decelerated in 2022 in line with tighter fiscal policy. But later reaccelerated again. Excluding some idiosyncratic contributions like Ozempic, or Boeing output fluctuations, or defense contracts, US GDP is already slowing from 2023 average pace.

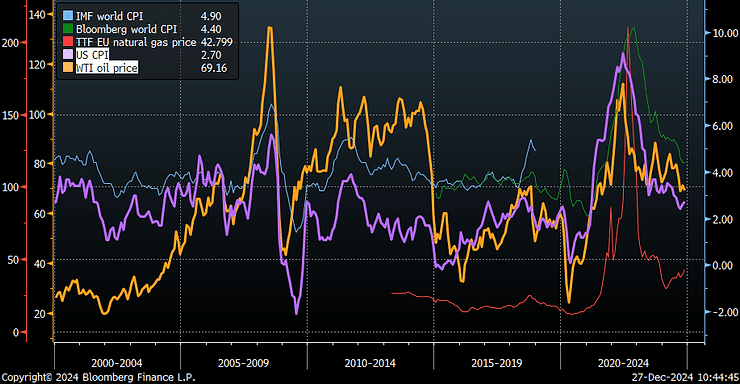

Global inflation declines. Absent of another forced closure of global manufacturing, 8% of GDP new fiscal impulse (both hardly possible), and (most importantly) energy shocks, inflation is set to decline further from here. Long term bond yields fall globally.

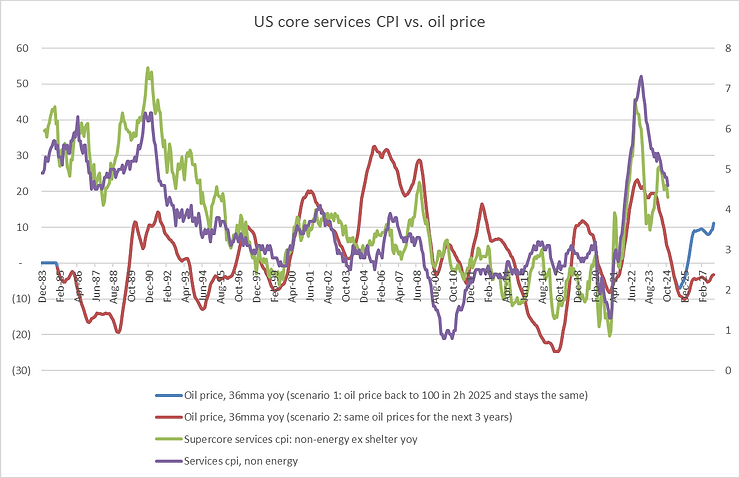

Inflation is closely linked to energy prices and usually moves in the same direction: shocks in 2008, 2014 and 2022 – are all interconnected, not just in the US, but globally too.

And oil/natural gas prices are not just part of headline CPI, but are important contributors to non-energy services ex-shelter CPI too. Energy plays a key role in services like transportation (air tickets), recreation (restaurants, beauty saloons), accommodation (hotels or short term rentals). In a scenario when oil prices stays the same for the next 3 years at $70/bbl, services CPI should be trending down. Unless oil jumps back above $100, the risk of the second wave of inflation is minimal.

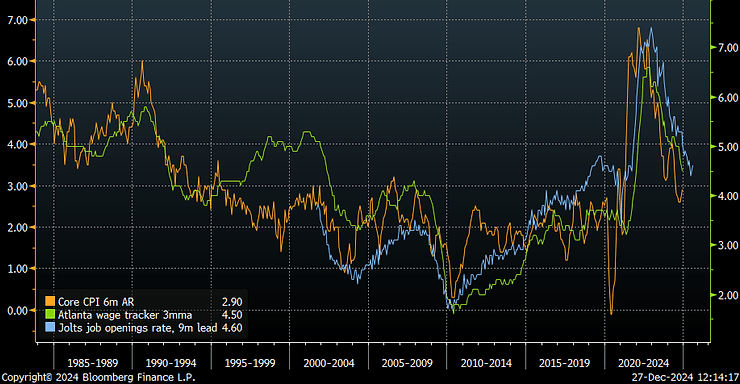

US wages, another potential source of inflation, are slowing down further, but are still above pre-Covid averages. However, US economy remains in the extended cycle top, and labor market will continue to soften.

Chinese economy is starting to pick up and perform better than expected, as consumer confidence rebuilds, economic stimulus spreads. China remains strong in car manufacturing, semiconductors, AI, energy technologies. Equities perform well next year.

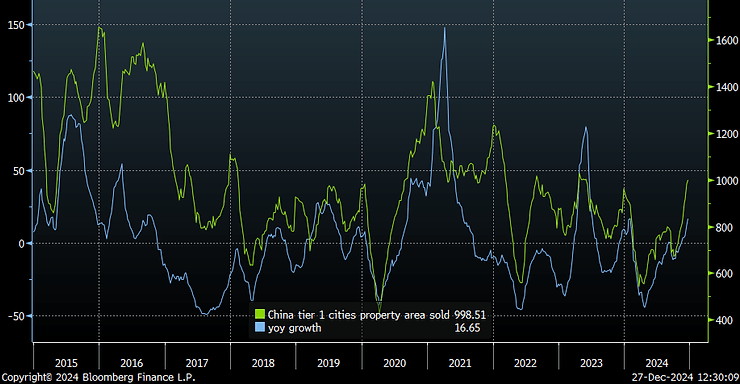

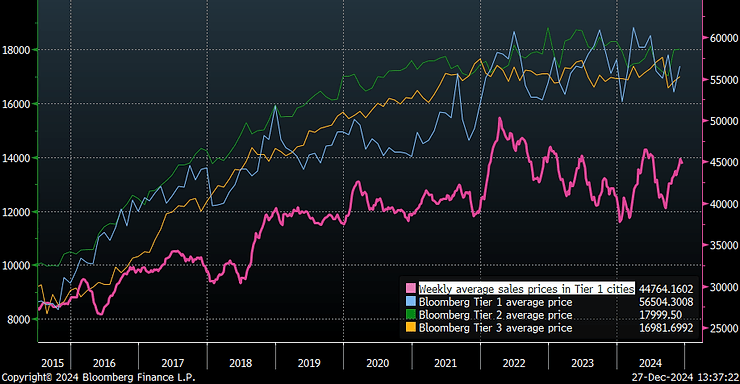

Property sales in tier 1 cities are rising.

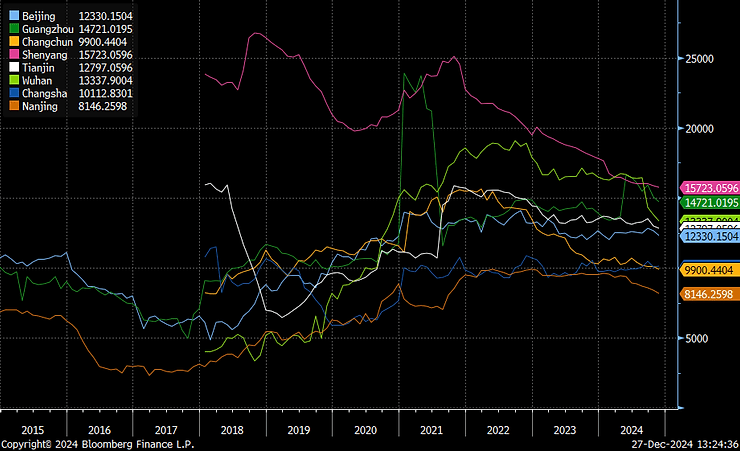

While supply of built properties is declining.

Aggregate weekly house values stopped declining.

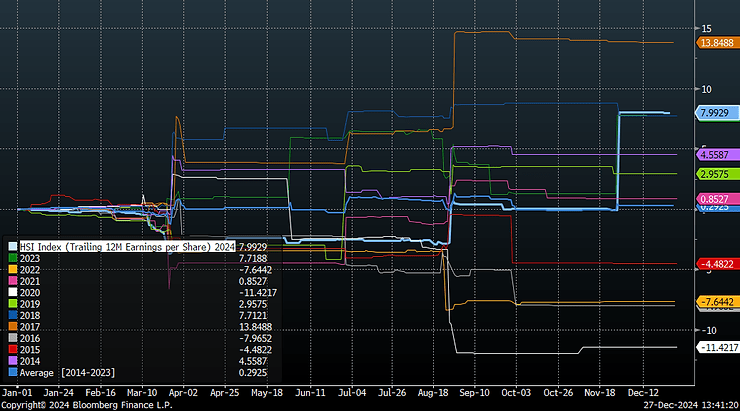

Corporate earnings are improving. HSI trailing 12m EPS is up 8% year-to-date.

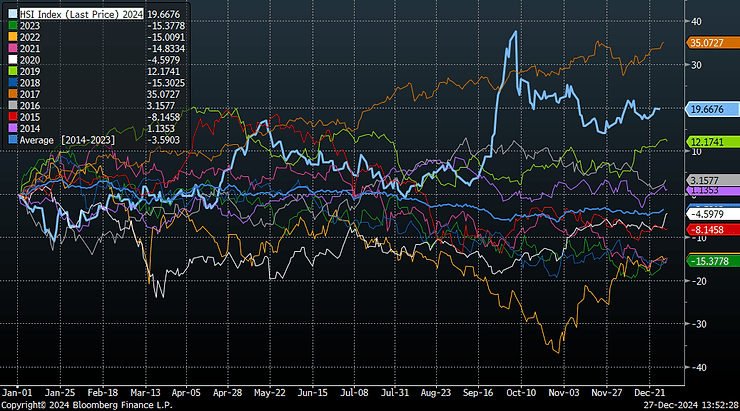

Equity market performance was also very strong compared to the last 10 years.

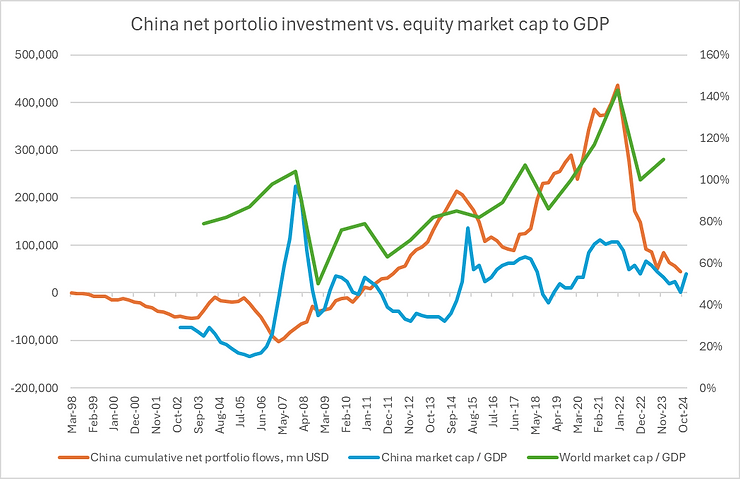

Net portfolio flows out of China have been negative since the end of 2021. Similarly China market cap to GDP peaked during the same period. It now stands at around 55%, compared to 110% of global market cap to GDP ratio. China is significantly underowned, while government is prepared to stimulate internal demand and the main source of deflation, property market, is showing signs of bottoming.

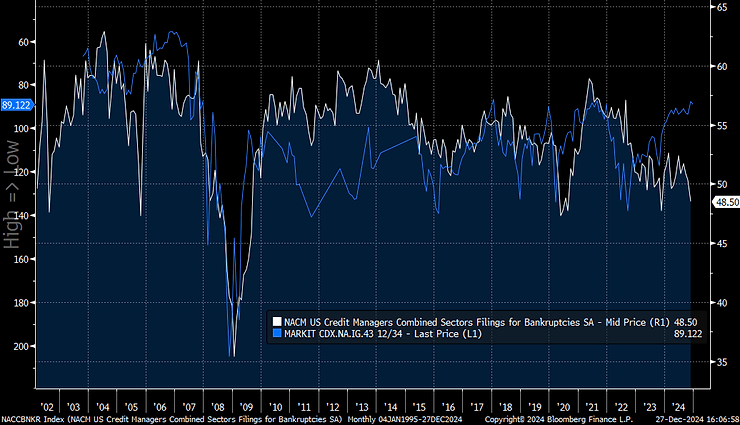

Defaults will get too costly to ignore: credit risk will jump.

Defaults are rising in various parts of the world and asset classes, while credit risk premium remains too complacent. Leveraged loans defaults and distressed exchanged are rising towards four year highs, as rates stay restrictive. And despite looser credit standards.

What are common characteristics of current US economy and the financial market in general? On the surface, yes, things are great, but constituents can look very weak.

S&P is making a new high every day? Yes, but breadth is worrying. Current negative breadth was associated with a major top during the dot com bubble or is usually a sign of market capitulation.

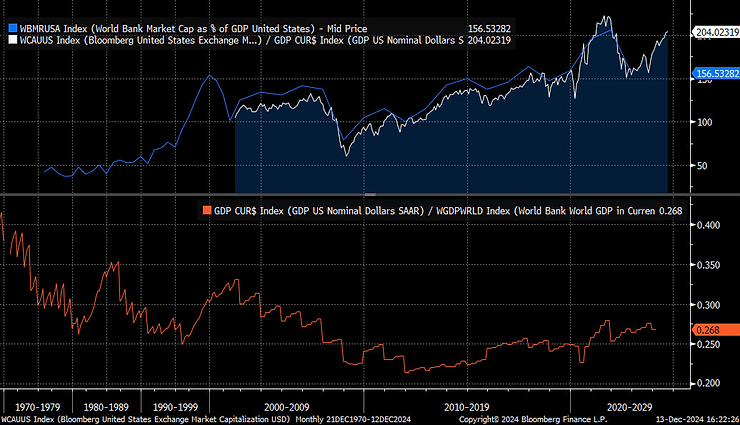

Now it’s becoming almost shameful to mention how expensive the stock market is. But divergence between US market capitalization to GDP and US contribution to global GDP is rising.

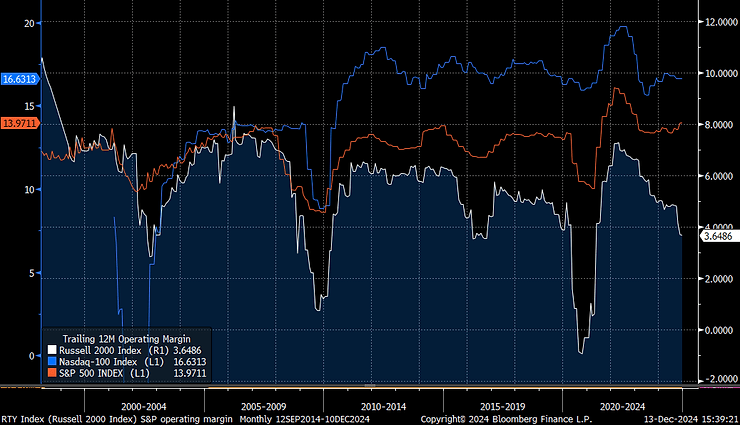

Corporate margins are record high? Yes for some, but not for smaller businesses:

Russell 2000 is also significantly underperforming S&P this year, especially compared to 2016, the first Trump election. Incremental policy benefit will be much smaller relative to the past.

NFP is rising to a new high every month? Yes, but according to household survey private employment declined by 1.3 million since the middle of 2023:

Number of people not on temporary layoff is accelerating.

Credit spread are making new lows? Yes, but number of bankruptcies is above pre-Covid level:

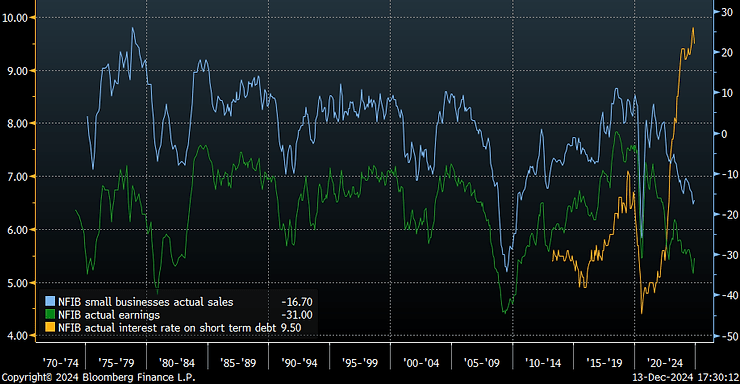

Small businesses are paying around 9% interest on their short term credit, while sales and earnings diffusion has collapsed.

Number of businesses losing money is rising:

The focus on aggregates disguises the fact that much of corporate America is in very poor shape. pic.twitter.com/0SSgKh7p2K

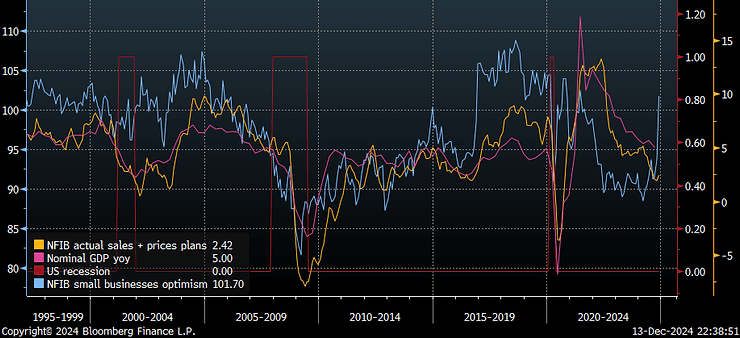

Expectations about Trump policy are super optimistic? Yes, but there’s still no pick up in current activity. Small businesses optimist jumped, same as in 2016. However, actual sales with prices (nominal GDP proxy) are declining this time.

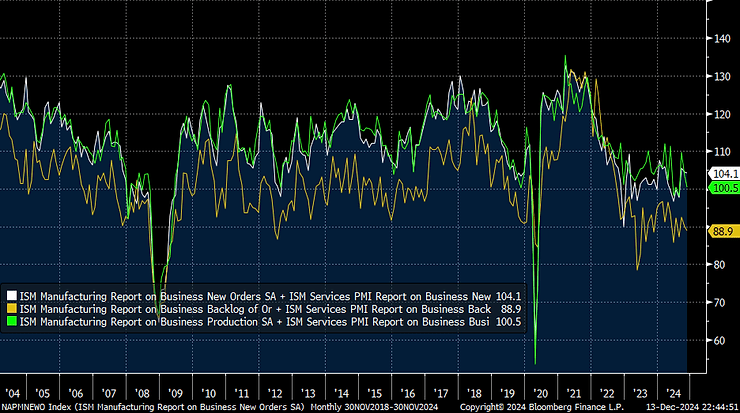

Combined manufacturing and services ISM new orders, backlog and output – all declined in November.

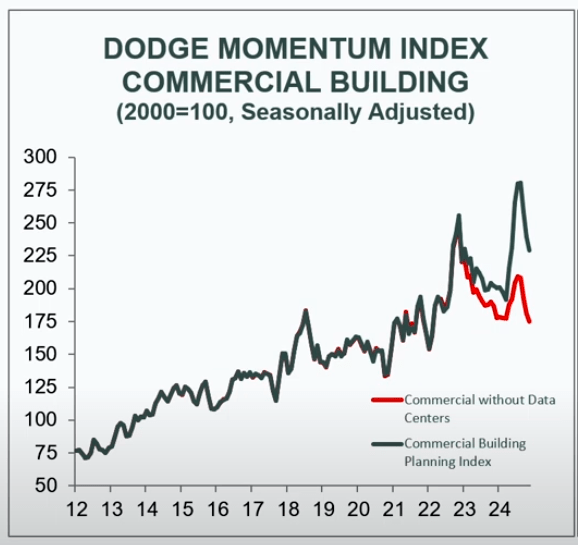

Commercial buildings construction leading index is also falling – capex cycle is turning lower.

Yes, US perceived exceptionalism is here, but equities are becoming very risky and bonds stay attractive just before consensus is pushing FED to take a pause.