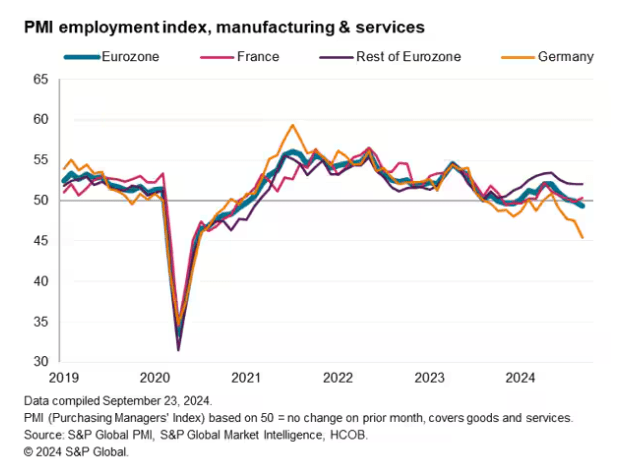

A number of really weak economic surveys are coming out from EU, while unemployment in Germany is spiking. Output continues to slide, while expectations are dropping quickly too, according to S&P Global:

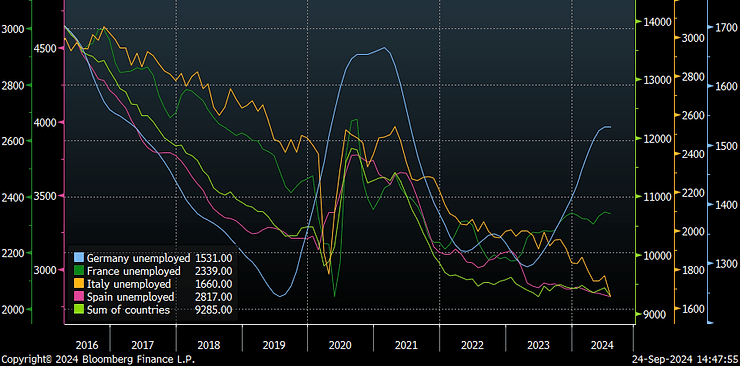

Unemployment is rising in Germany and France, expectations are deteriorating as well. Lower unemployment in Italy and Spain help keeping overall EU unemployment smaller.

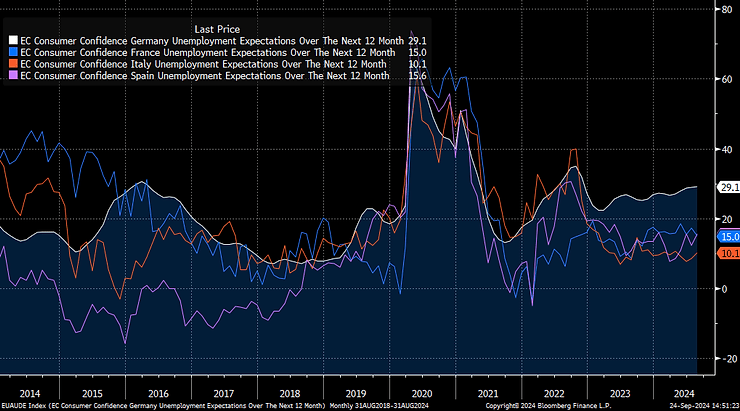

Consumer unemployment expectations are slowly picking up further.

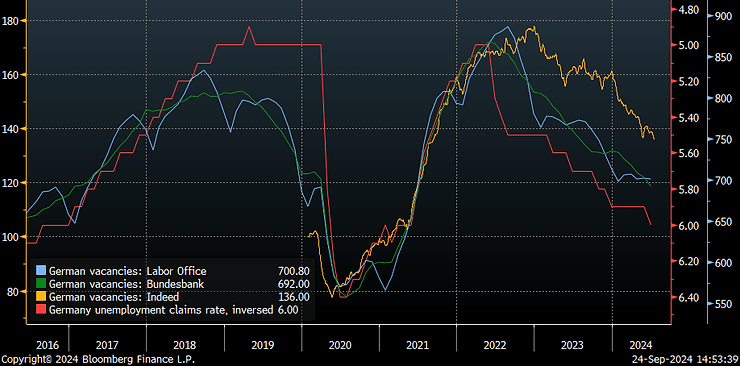

German vacancies are collapsing to absolute levels of 2015-2016.

More companies in Germany are reducing their workforce and VW is not alone – just a couple of months after IG Metall demanded a 7% wage increase.

Overall EU car registrations collapsed 18% year over year in August and ZEW points to more downside here.

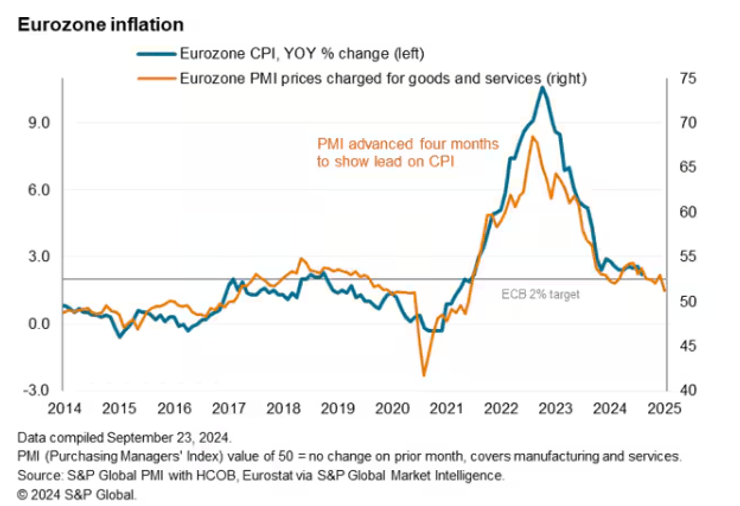

Price pressures are easing at the same time in both manufacturing and services, even though motor insurance can continue to have an outsize effect on average services inflation.

Eurozone economic surprise index reversed this week and corporate earnings revisions are deteriorating.

German short term yields are starting to catch up with US move, which should probably continue. And bad news should be bad news for equities too.