First, 2025 review. Recession didn’t happen. At least when you look at financial markets. And ignore unemployed. Common theme by the end of the year formed as: “there’s not enough exuberance about AI“. More detailed view below. And yes, risk of US recession is still high.

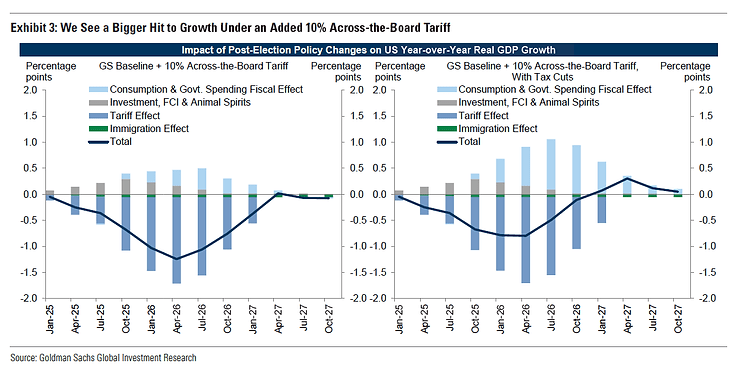

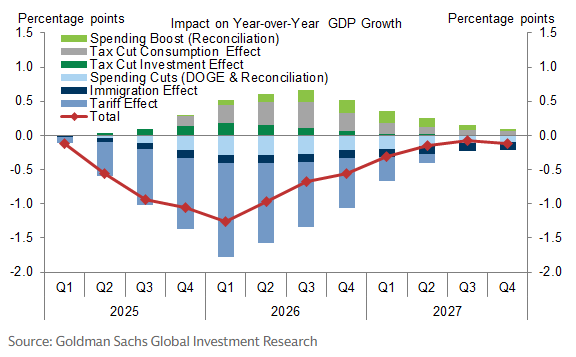

- US economy. Tariffs. The risk of tariffs GDP drag is skewed to the downside due to the Supreme Court decision as well as poor Republicans pre-election odds. And of course Trump’s $2,000 rebate proposal. Nevertheless, status quo tariffs impact on GDP is offsetting the frontloaded stimulus that is kicking in soon.

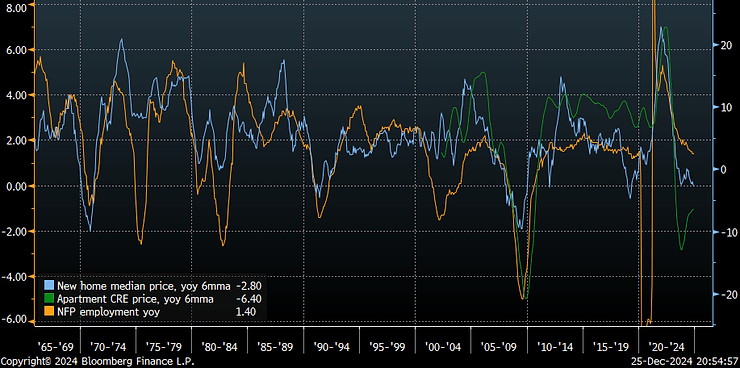

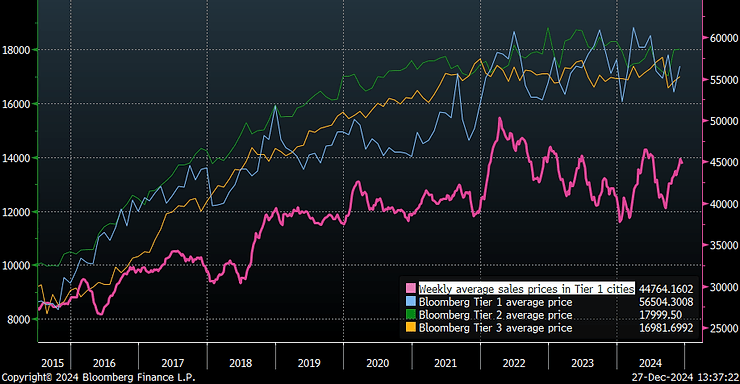

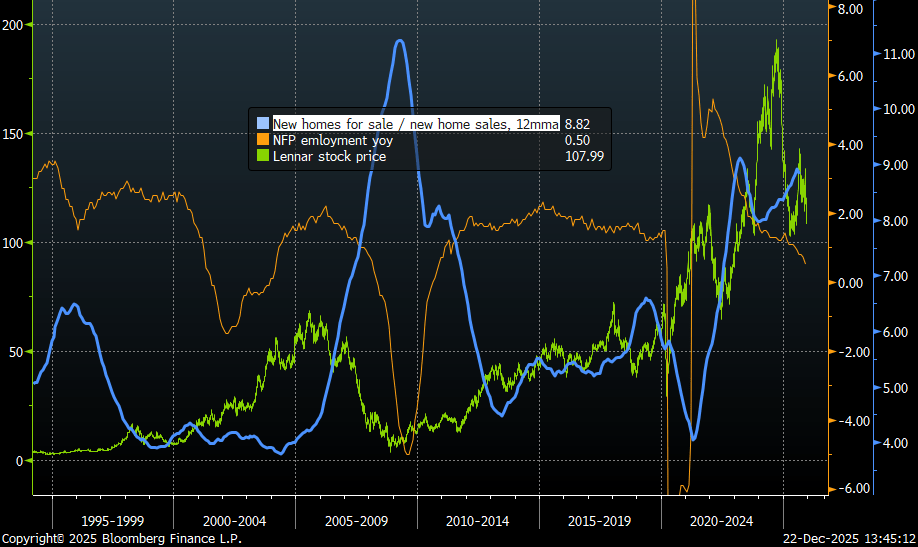

Housing market. Inventory of available housing is rising. Homebuilders earnings expectations are collapsing, dragging down their share prices. Housing will remain in oversupply in 2026 and prices will be softening.

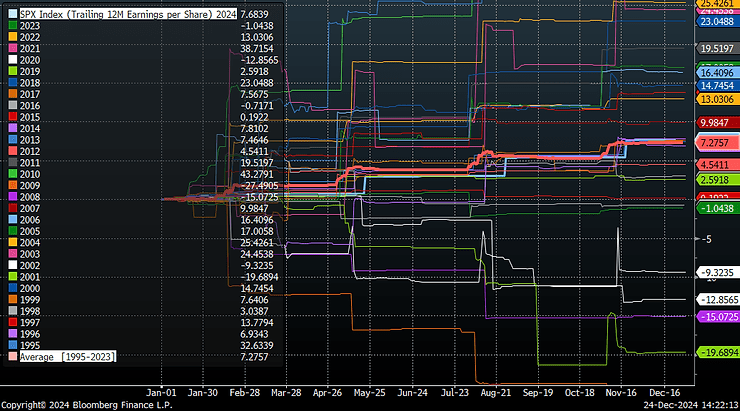

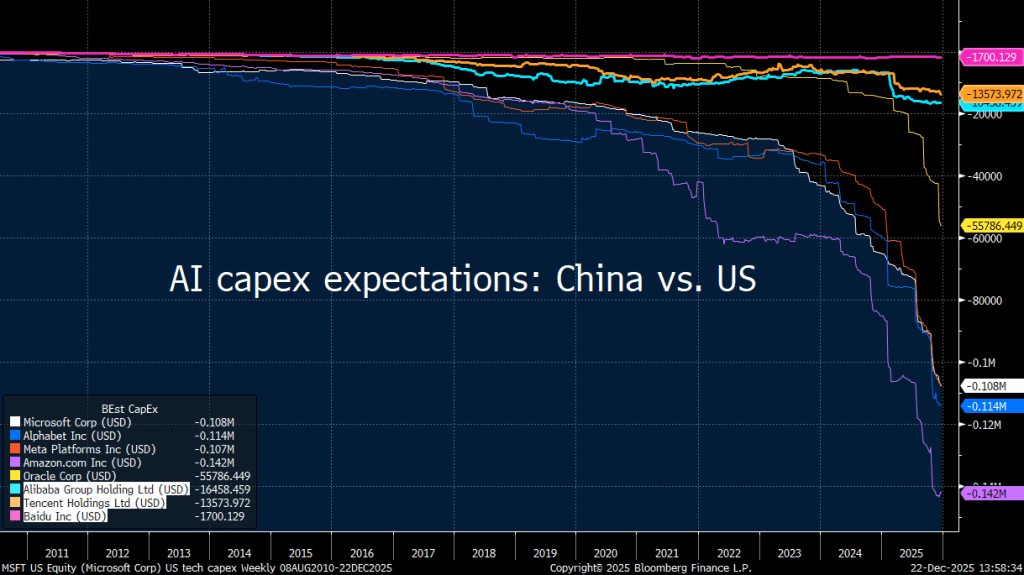

Business capex. AI spending proved to be much stronger than expected despite rising AI competition. Competition is increasing from Chinese models or the rise of alternative compute methods. Scale, rather than optimization/research/monetization is the main AI driver now. The part that can be sold easier.

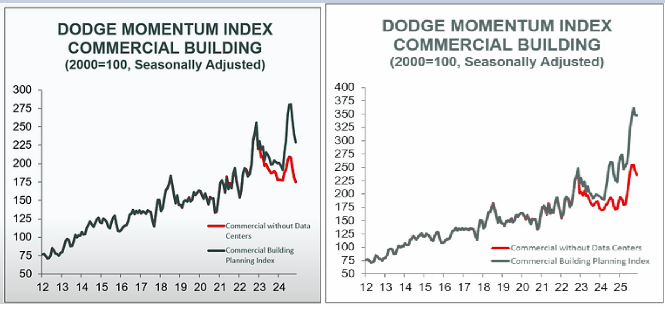

Actual data centers spend is spreading beyond just tech companies. Commercial building construction index year ago and now. What seemed as a slowdown, was just a pause. As building a data center seems to be an easy business pitch.

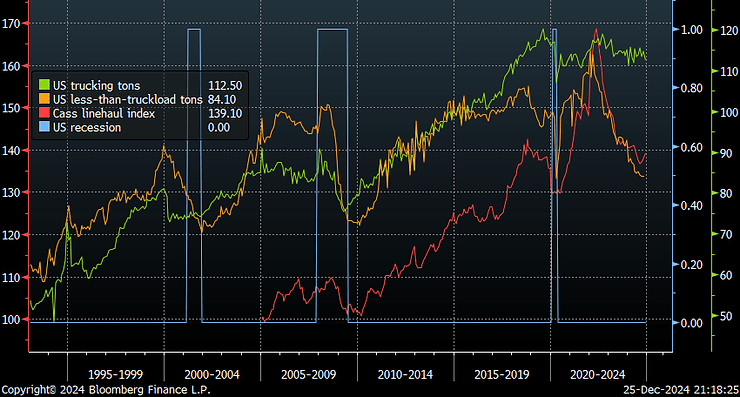

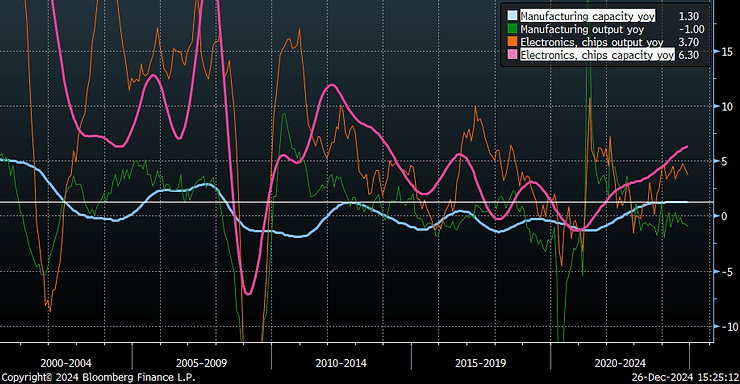

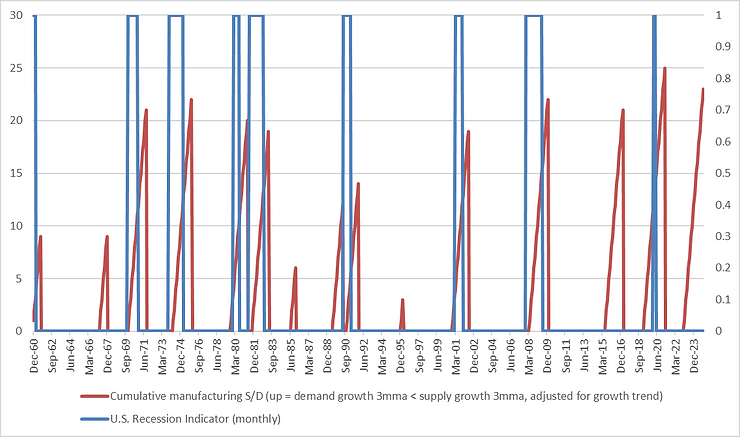

Meanwhile, real median US manufacturing is contracting. Number of industries with output rising more than 3% pear year is near recession levels. AI revolution is concentrated in a few sectors at the moment. Unlike previously stronger manufacturing periods like tax cuts (2018), shale (2014), housing (2005)or internet (1999). Interestingly, tariffs so far had minimal impact on domestic output.

Capex expectations are also significantly different between AI and the rest. Outside of the hyperscalers, companies aren’t planning to increase (nominal!) capex in this cycle.

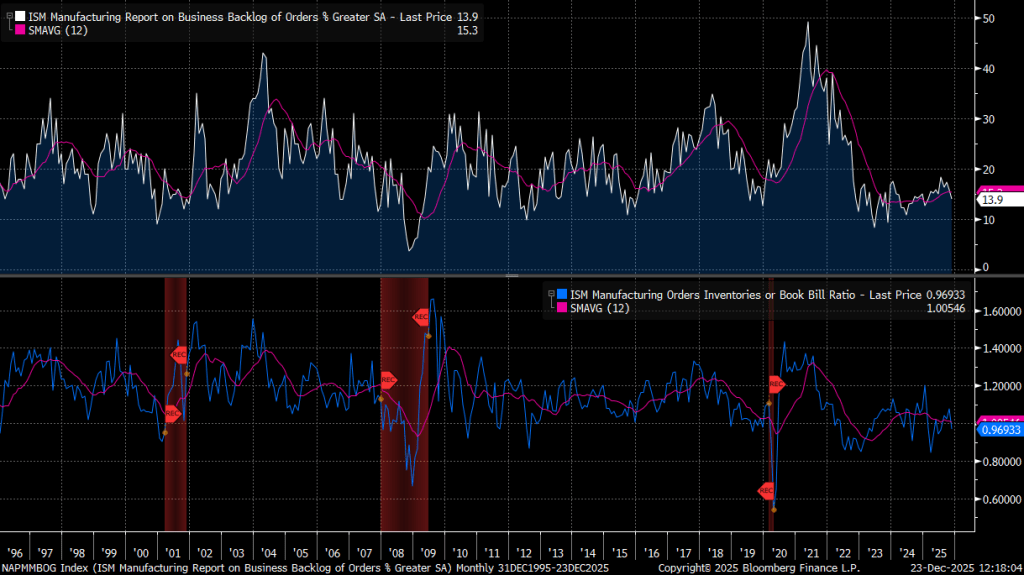

ISM business backlog is depressed, book-to-bill ratio is at recessionary levels. Manufacturing recession keeps rolling across the sectors.

Also, AI capex starts to be perceived as a drawback, judging by Oracle share price and CDS spread, or by reaction to capacity cancellations. Risk of lower than expected AI capex is rising.

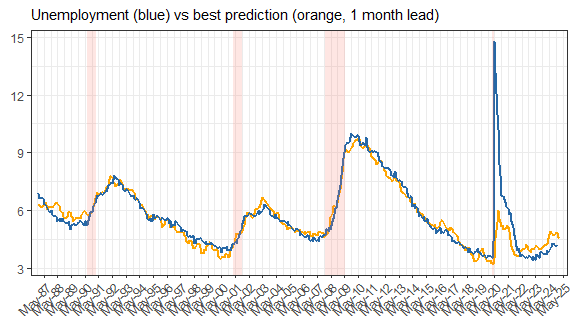

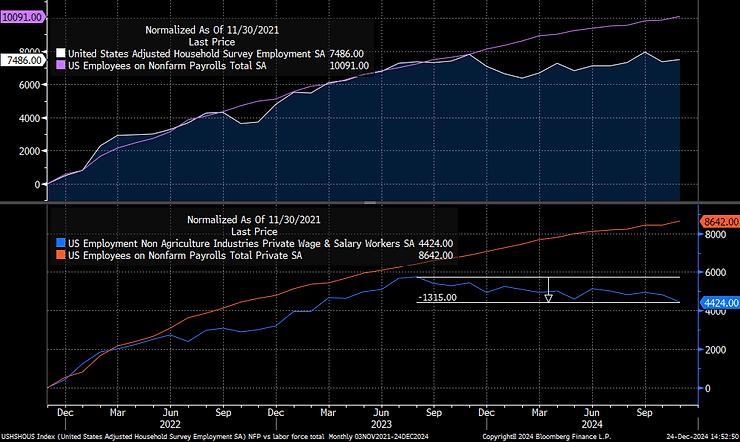

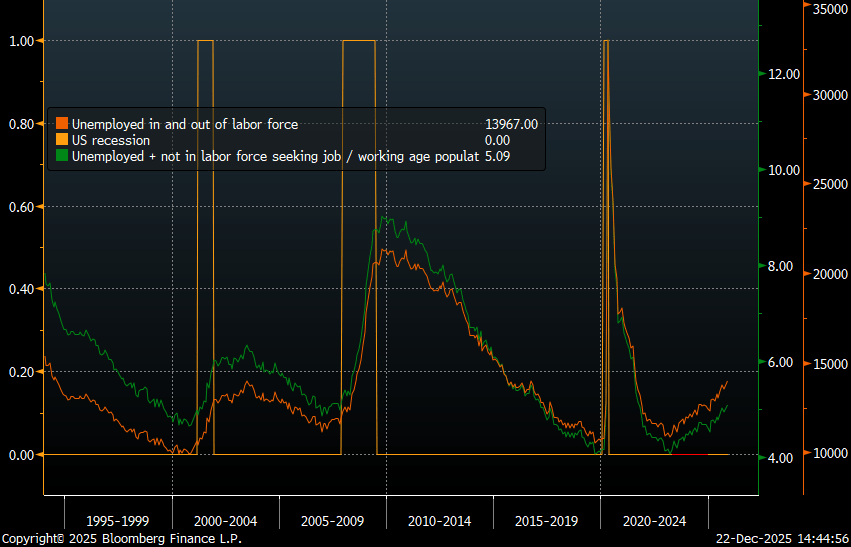

Unemployment. It’s rising as expected and will increase in 2026. Number of people without a job is growing – either in or outside of the labor force. Weak housing market and capex won’t help next year.

Small companies continue to see weak sales ahead, while consumers fell poor labor conditions. That’s usually a sign of higher unemployment.

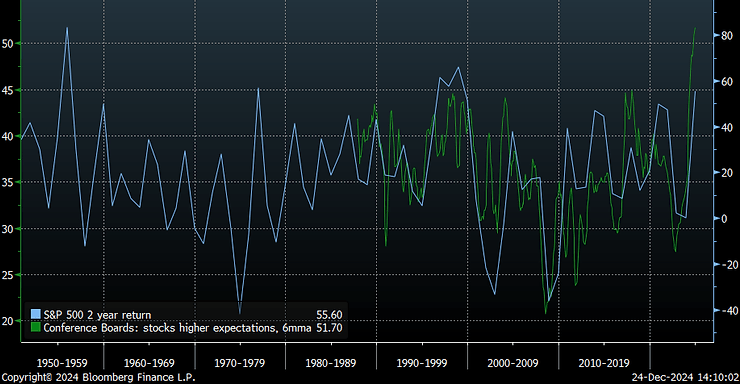

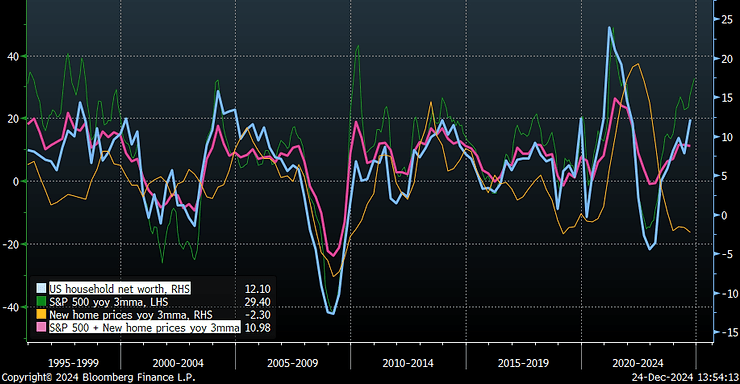

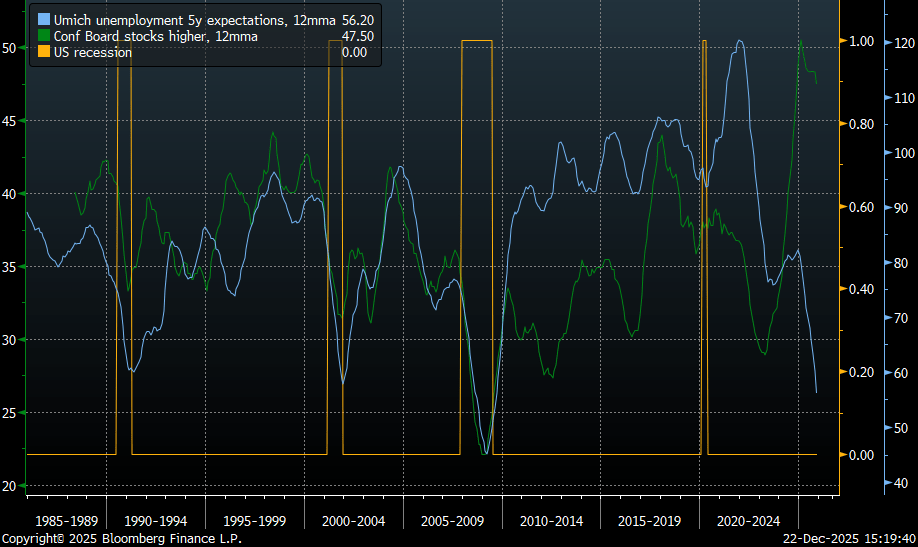

Wealth effect. Probably that’s the core reason of stronger than expected consumption in the US. The spread between consumers unemployment expectations and stock market expectations is the largest ever. Everyone has to be invested in (AI) stocks and hope your job isn’t cut. Wealth effect will decline due to weaker equity and housing markets next year, probably.

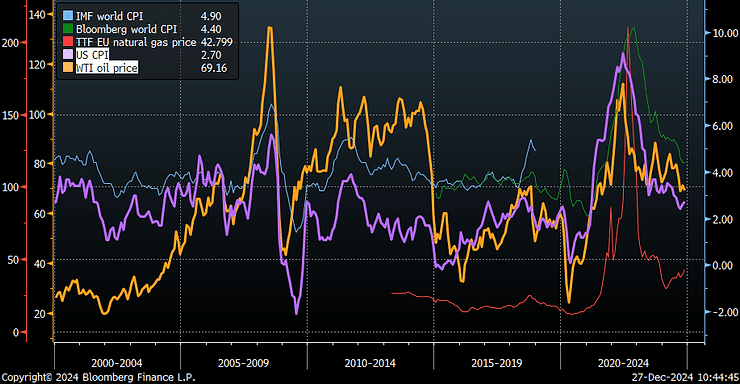

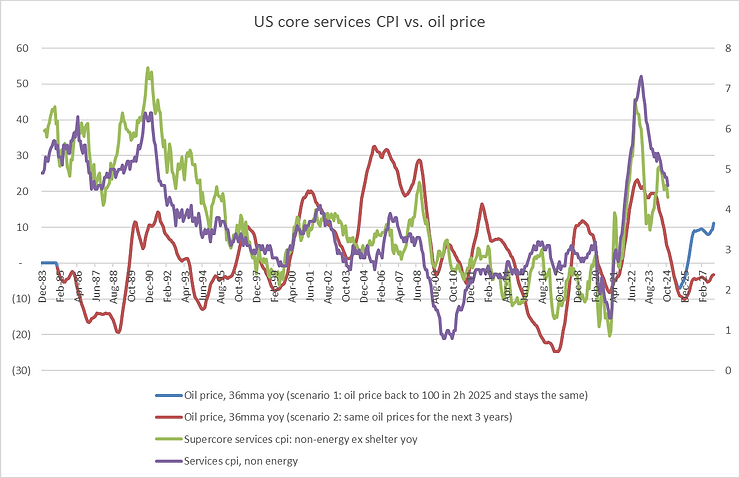

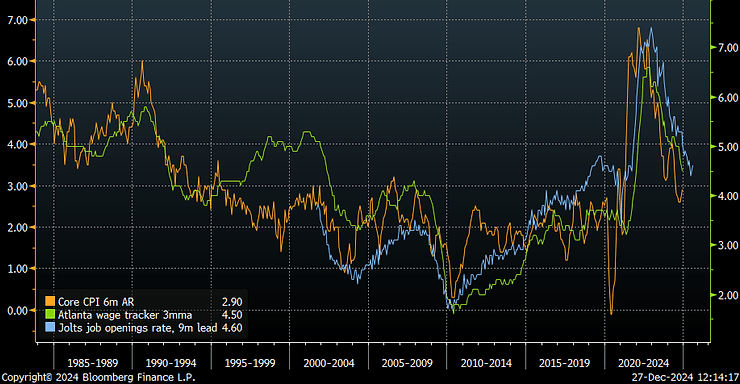

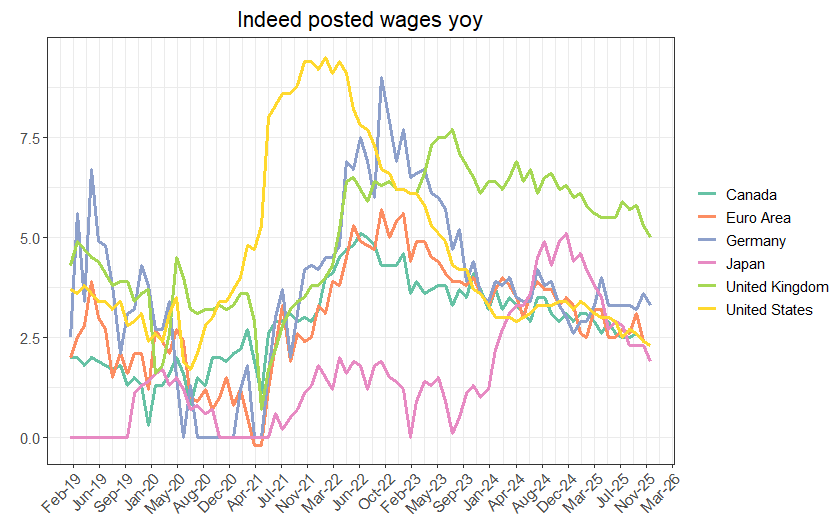

2. Global inflation declines. This proved to be correct. But it’s mostly visible in EMs, rather than DMs, where inflation is higher. Tariffs were deflationary for the world. Effect of strong wages in developed markets is more pronounced than in EMs, after decades of relatively low wage growth.

At the moment, DM wages are slowing down, led by the USA. Japan is still experiencing inflation problem, but wages there have rolled over already. Next year inflation will be lower again.

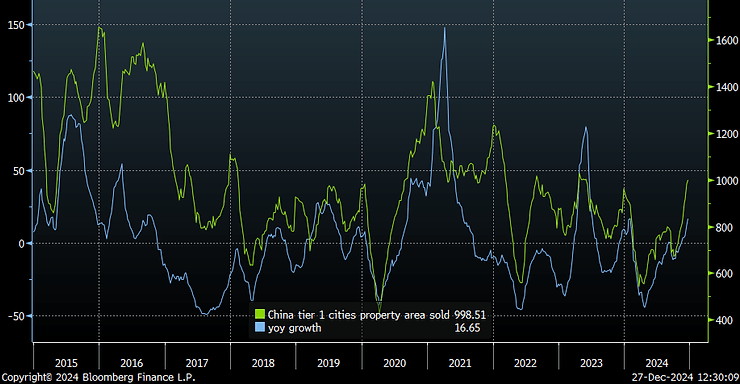

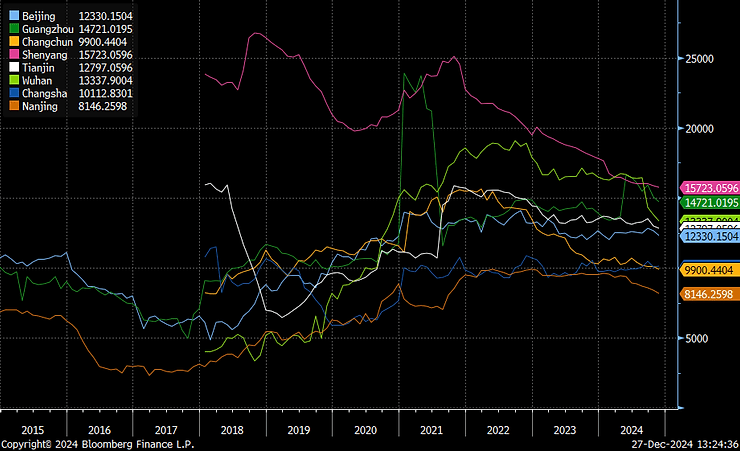

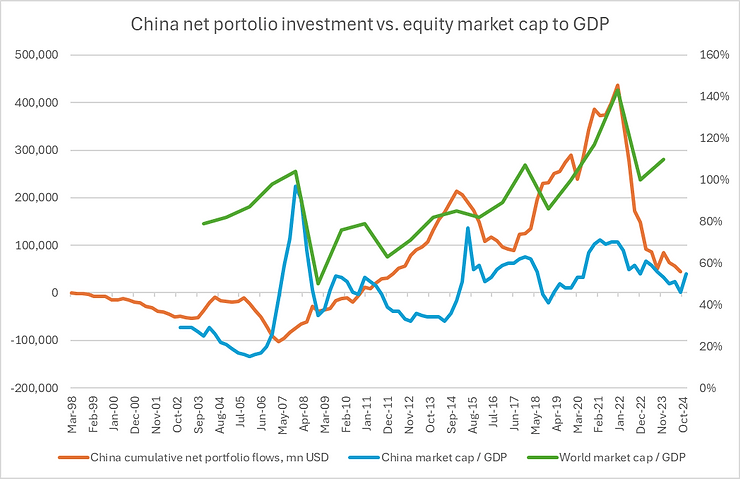

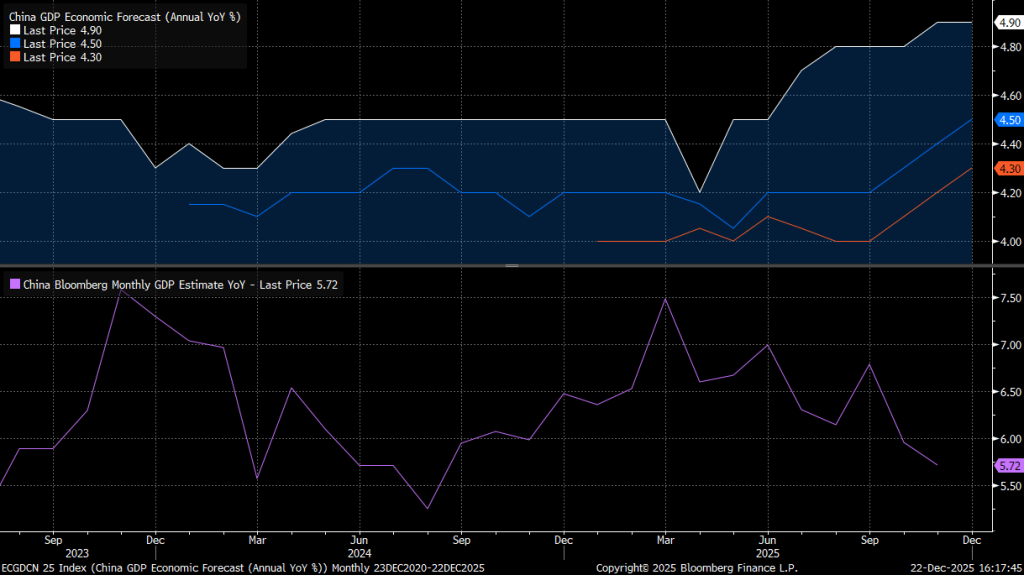

3. China economy performs better than expected. China GDP growth expectations are in fact rising while housing market is still deteriorating.

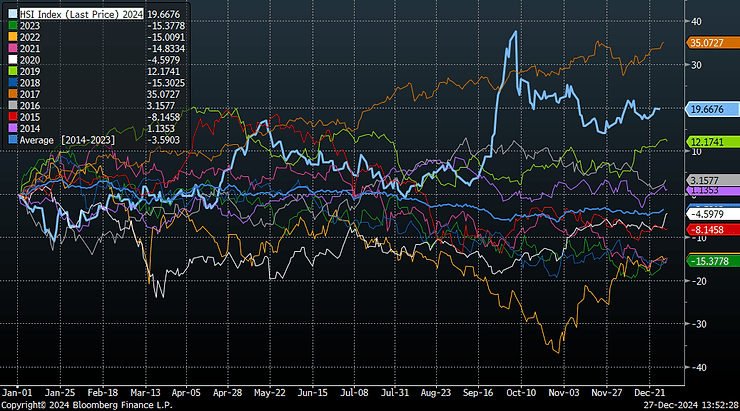

Stock market has also rallied, but of course not that great as Kospi or even Ibex.

But the next year is going to be more challenging as lending is deteriorating going into 2026, unlike 2025. Strategic sectors, like chips, electrical equipment and renewables should outperform next year.

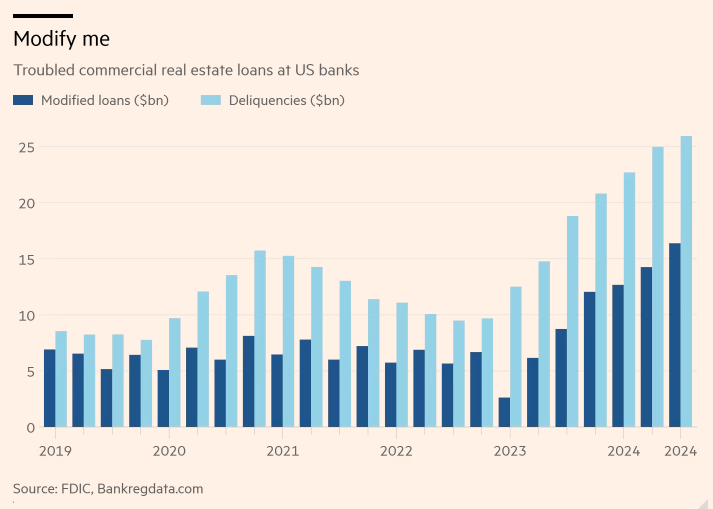

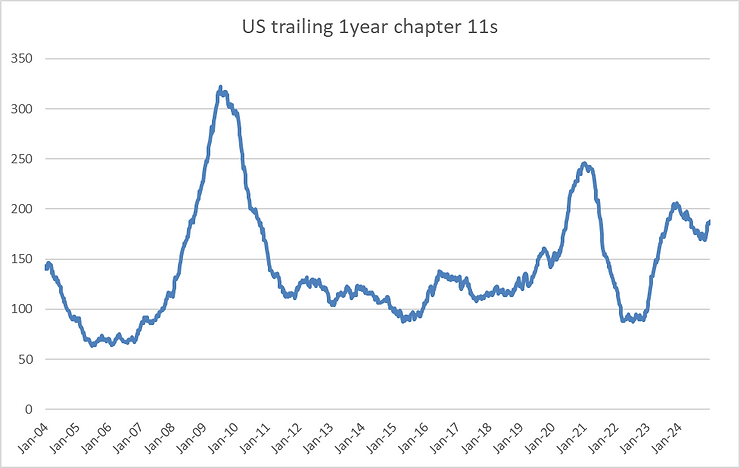

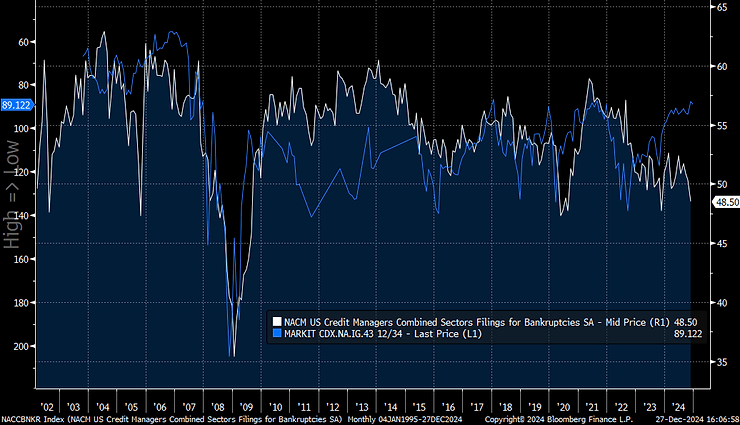

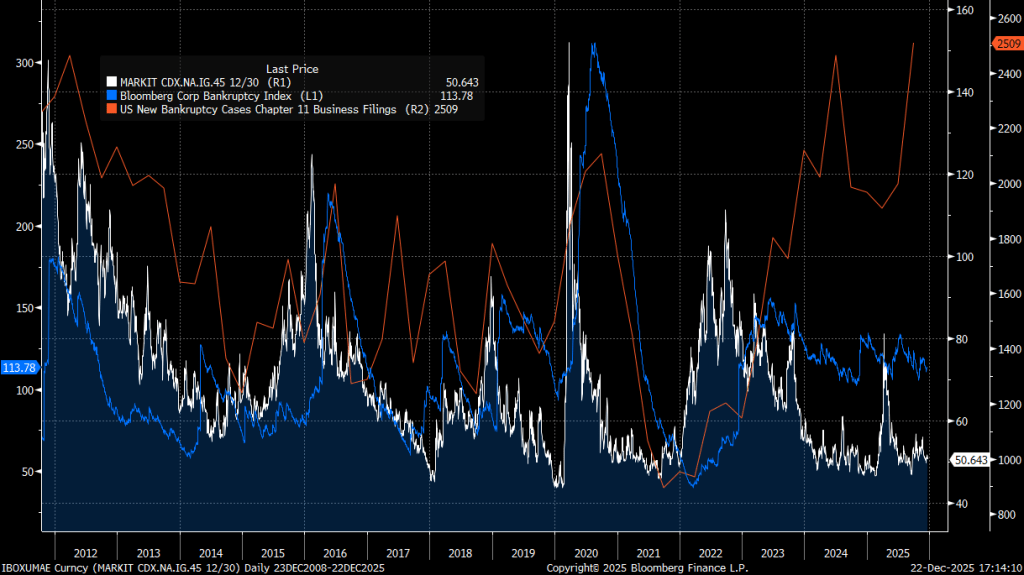

4. Higher number of defaults didn’t translate into higher credit spreads. In fact, actual number of defaults is making new highs every quarter. That’s in line with weaker small business sales expectations and consumers job fears. Spreads will have to crack in the end, either public or through private credit channels.

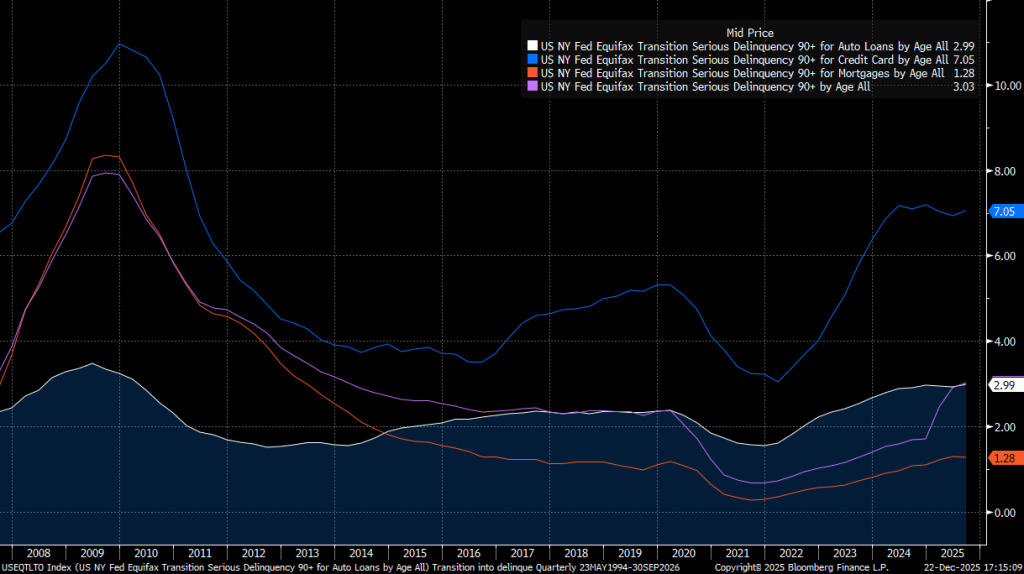

Consumer delinquencies are deteriorating as well. Credit short has been a poor recommendation. It was relatively more resilient during the liberation day sell off too.

5. Performance. Overall, recommendations performance was unsatisfactory. HSI outperformed S&P, but S&P is still up 18%. Liberation day ended up better than feared for the stock market, but didn’t help the economy. Long term treasuries returned only 4% in 2025 with significant volatility. Other DM bonds performed even worse. Front end of the treasury curve was a good trade, but it was offset by strong corporate credit performance.

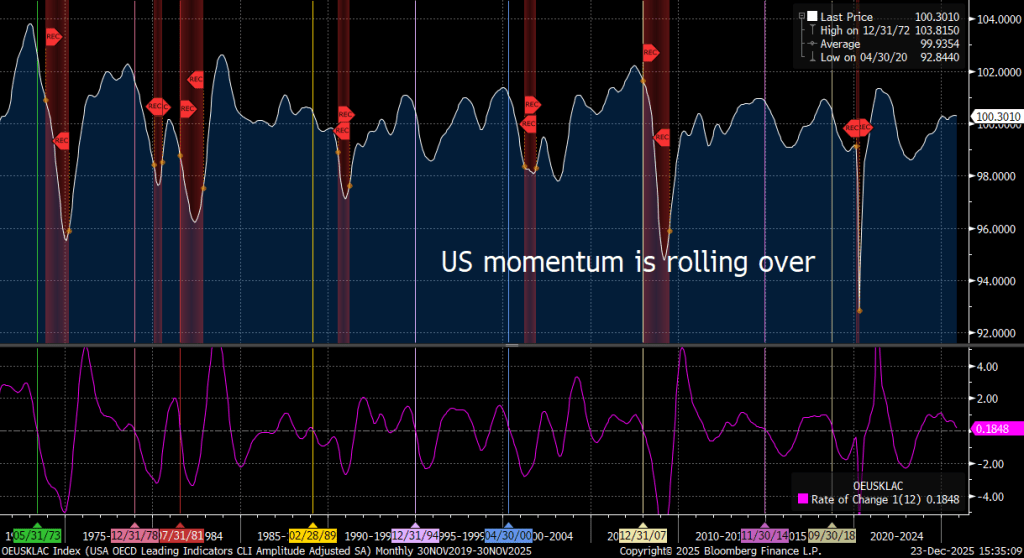

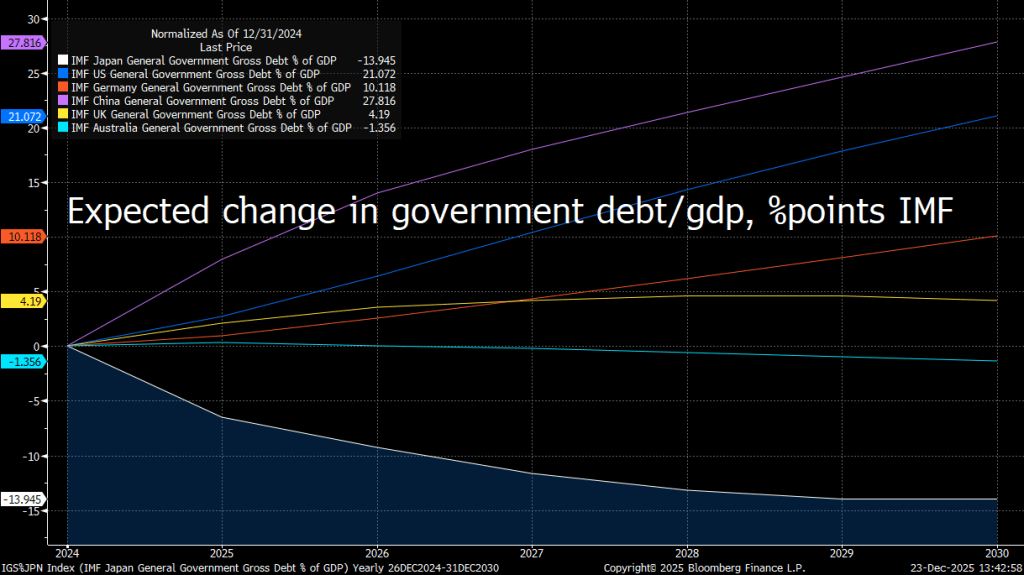

6. 2026 predictions. Inflation won’t be a problem. Jobs – will. Unemployment should rise and consumption decline. And S&P should be down on a year, as AI will disappoint. Global growth is about to peak as well. In that case the risk of another fiscal package is increasing.

In this scenario front end rates DM will continue to rally. JPY and JGBs will rally too, as inflation declines and domestic players start to hedge currency again.

Happy New Year.