What are common characteristics of current US economy and the financial market in general? On the surface, yes, things are great, but constituents can look very weak.

S&P is making a new high every day? Yes, but breadth is worrying. Current negative breadth was associated with a major top during the dot com bubble or is usually a sign of market capitulation.

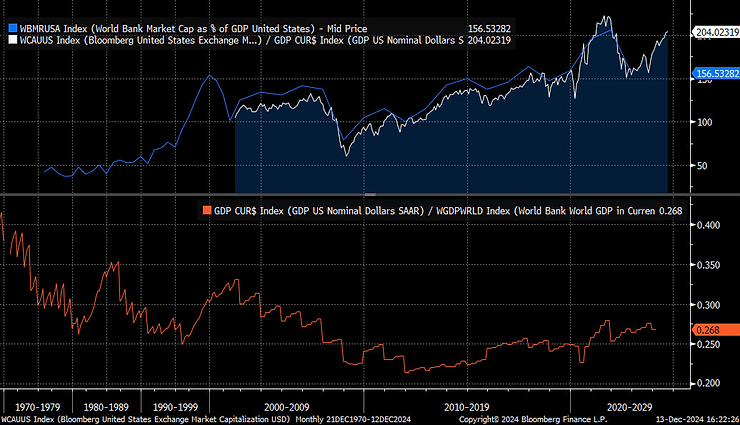

Now it’s becoming almost shameful to mention how expensive the stock market is. But divergence between US market capitalization to GDP and US contribution to global GDP is rising.

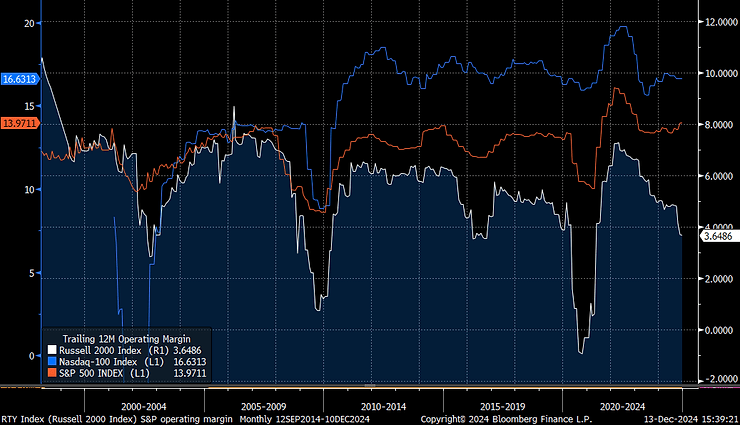

Corporate margins are record high? Yes for some, but not for smaller businesses:

Russell 2000 is also significantly underperforming S&P this year, especially compared to 2016, the first Trump election. Incremental policy benefit will be much smaller relative to the past.

NFP is rising to a new high every month? Yes, but according to household survey private employment declined by 1.3 million since the middle of 2023:

Number of people not on temporary layoff is accelerating.

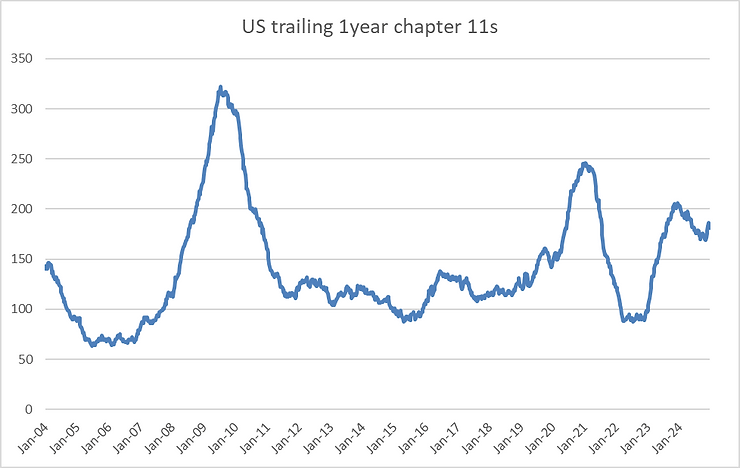

Credit spread are making new lows? Yes, but number of bankruptcies is above pre-Covid level:

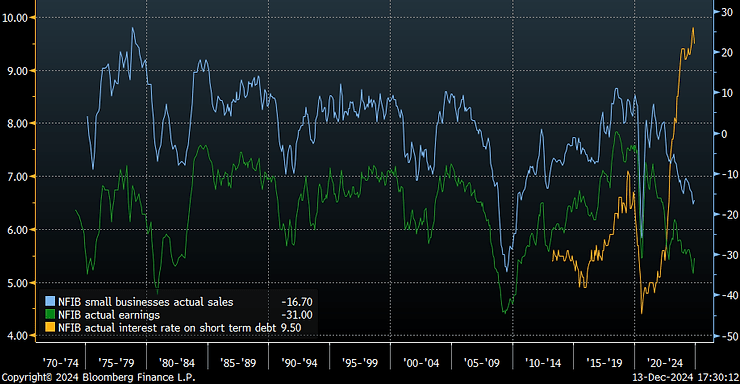

Small businesses are paying around 9% interest on their short term credit, while sales and earnings diffusion has collapsed.

Number of businesses losing money is rising:

The focus on aggregates disguises the fact that much of corporate America is in very poor shape. pic.twitter.com/0SSgKh7p2K

— Peter Berezin (@PeterBerezinBCA) December 13, 2024

https://platform.twitter.com/widgets.js

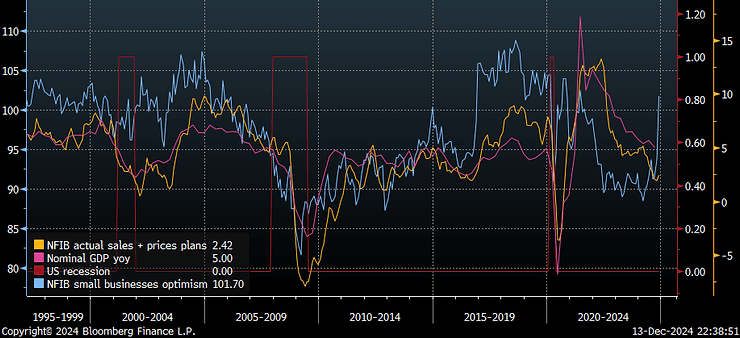

Expectations about Trump policy are super optimistic? Yes, but there’s still no pick up in current activity. Small businesses optimist jumped, same as in 2016. However, actual sales with prices (nominal GDP proxy) are declining this time.

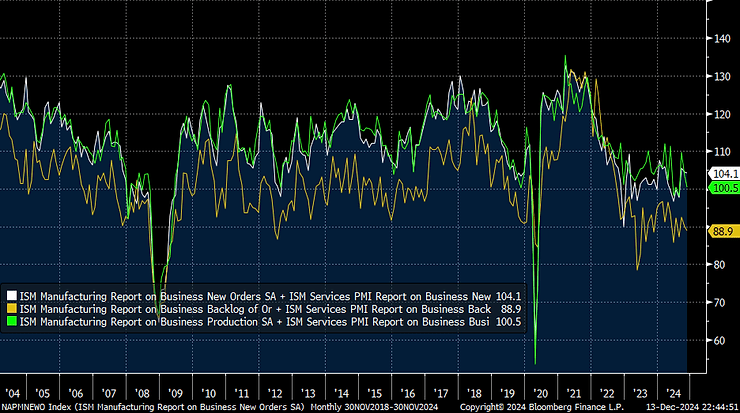

Combined manufacturing and services ISM new orders, backlog and output – all declined in November.

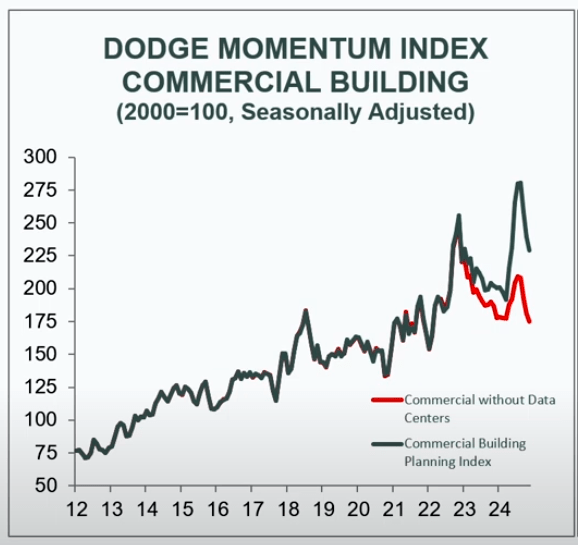

Commercial buildings construction leading index is also falling – capex cycle is turning lower.

Yes, US perceived exceptionalism is here, but equities are becoming very risky and bonds stay attractive just before consensus is pushing FED to take a pause.