Inflation continues to miss expectations and labor market apparently has been weak since April, judging by the large NFP revisions. Tariffs prove to be a catalyst for a slowdown in US economy, but not in US (AI) stocks yet.

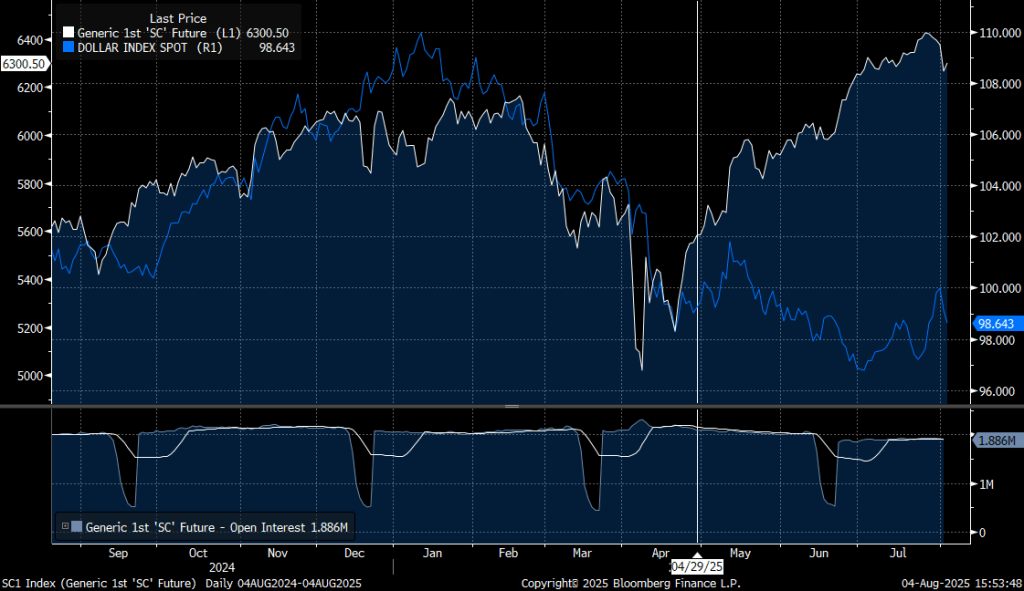

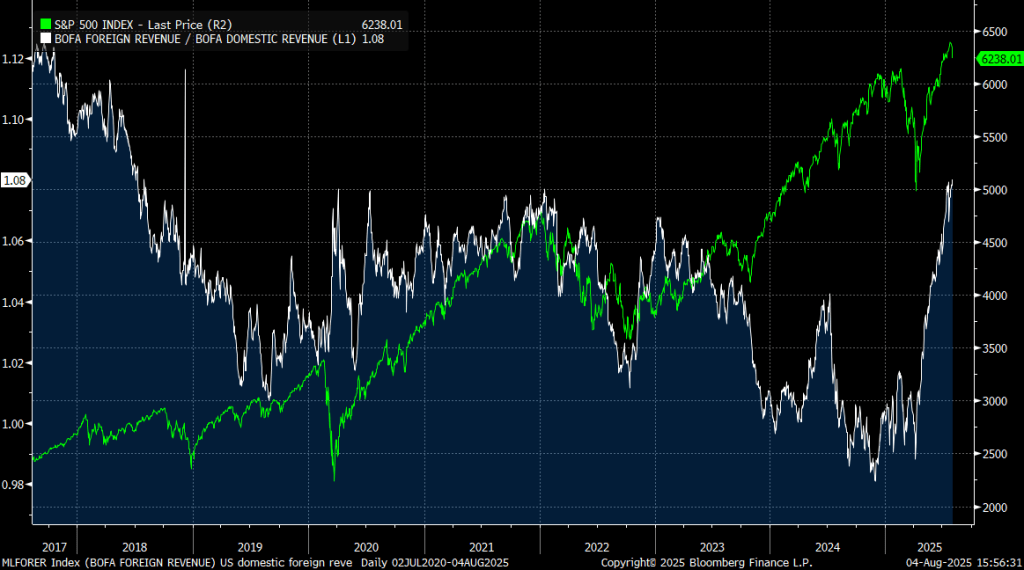

US companies report relatively healthy earnings, as dollar weakens and US avoids retaliatory export tariffs.

Exporters are leading the latest upward leg in US stocks. US Tech will probably avoid additional foreign taxes as well – as a part of the same deal.

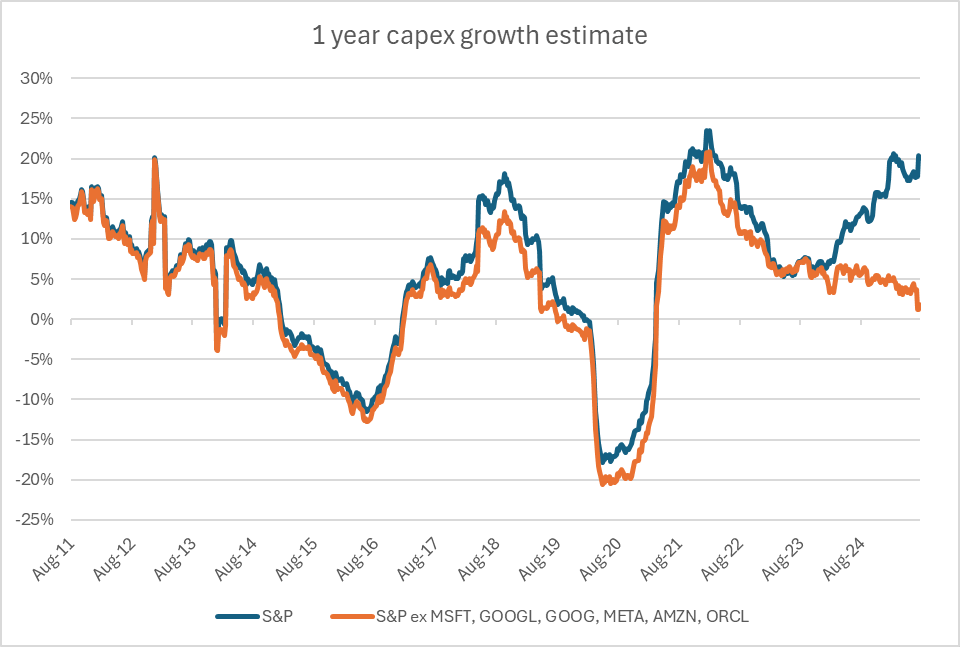

US Tech continues to expand AI capex, while the rest of the S&P 500 index is reducing capex growth to almost 0. Compositionally that’s not great for the labor market going forward, since big tech basically stopped hiring after Covid, but other business didn’t.

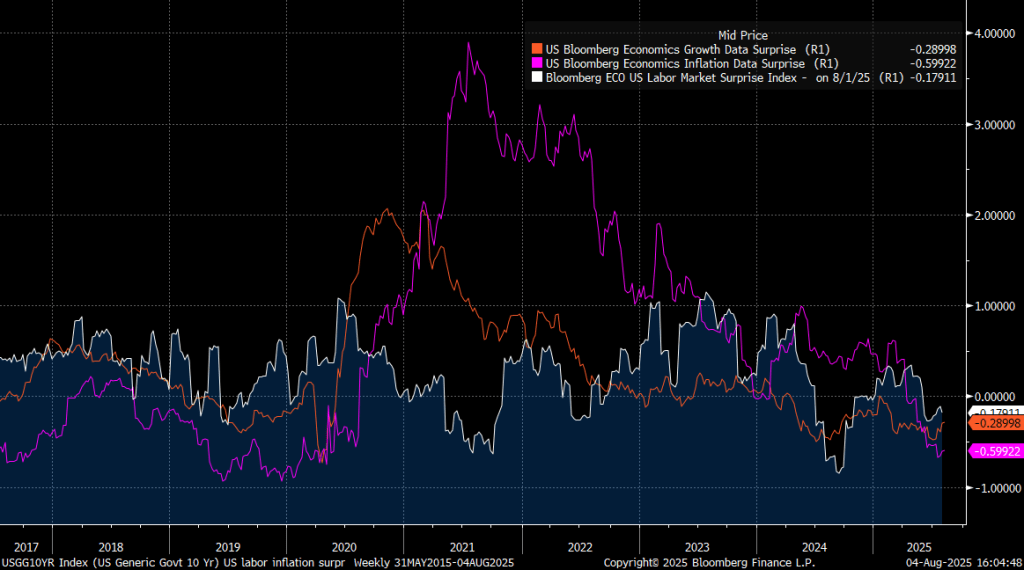

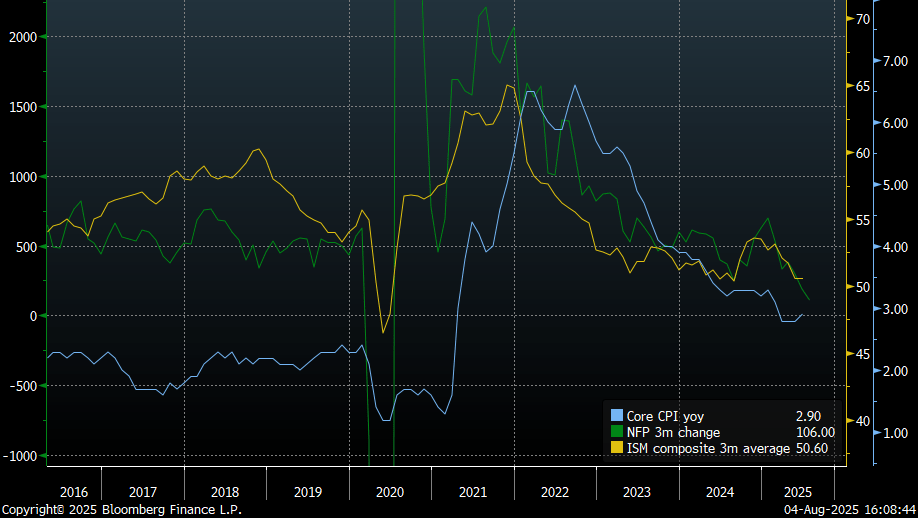

At the same time US economic data continues to surprise negatively on aggregate. Growth, labor, inflation – weaker than expected.

All three parts of the economy continue to slowdown. Labor is contracting now.

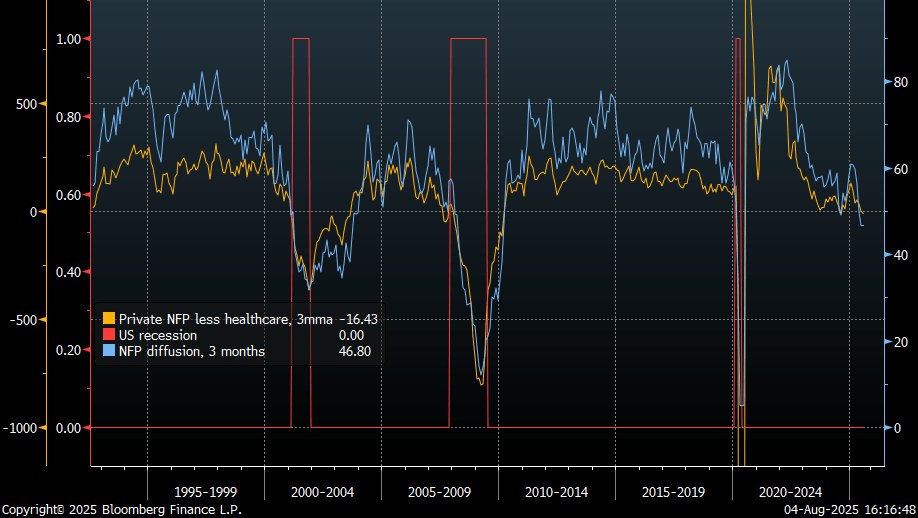

Absolute number of NFP jobs created as well as jobs breadth has deteriorated substantially – now also worse than in summer 2024 and in line with recessions.

Unemployment, including people who are not in the labor force but want a job, is rising at the similar trend as in the last couple of years. Albeit slower than in 2000 and 2008, as layoffs are still low. AI hasn’t altered the trajectory yet.

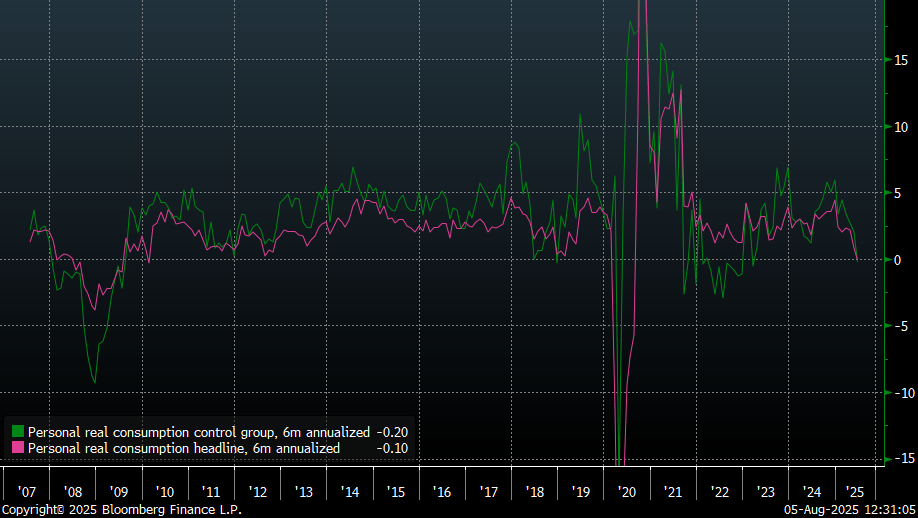

US personal consumption slowed down substantially this year as well. Household are saving more, as labor market uncertainty is rising. And number of jobs is declining.

There are signs of AI cycle slowing down from here too, despite ever rising capex plans. While Taiwanese orders and exports are booming, soft leading indicators are souring.

Central bank easing options continue to look attractive. Long term yield found some resistance, making duration more favorable. DM equities are facing downside risks, as export economies will suffer from the “trade deals”, and in US consumer is losing steam.

Leave a comment