Newly released economic data out of US is rolling over quickly. At first glance, Trump tariff policy and Doge employment actions are raising uncertainty and reducing activity. In fact, economy has already been showing topping signs for a while. Lack of layoffs and aggregate corporate earnings were key pillars of the current cycle. But this might be unwinding at the moment.

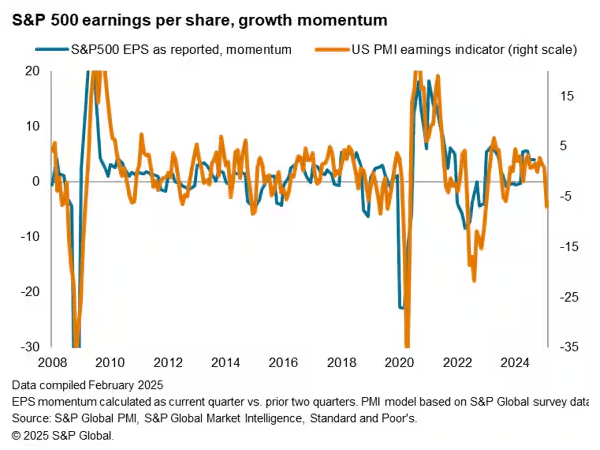

Corporate earnings are now facing downside risks, according to S&P.

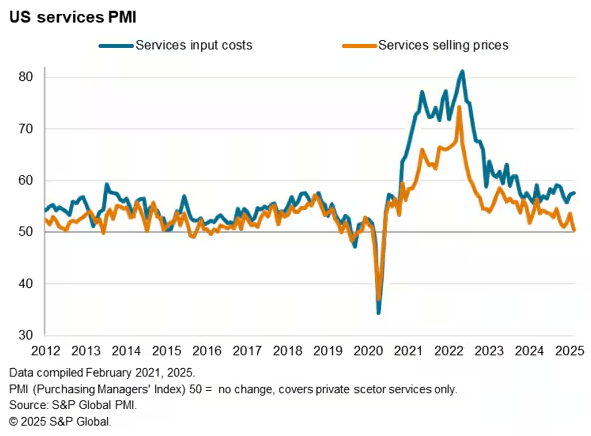

As service companies aren’t able to raise prices anymore.

Diffusion of earnings-per-share expectations has been deteriorating. More S&P sectors are expected to have declining earnings over the next 12 months. This can trigger a sell off in equities.

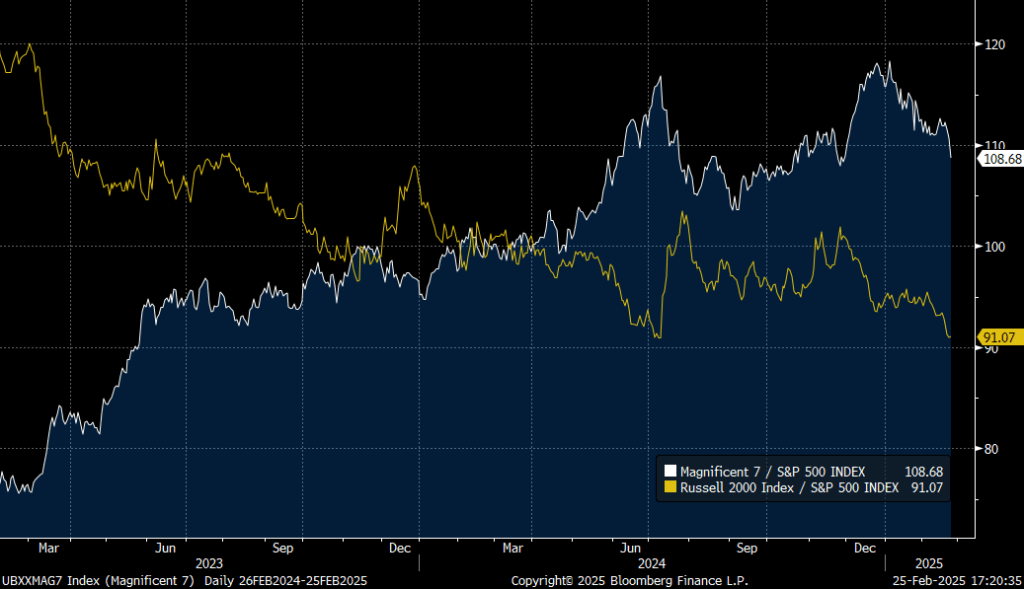

Largecap AI story is not only shaken by the Deepseek news, but by new potential reversal in activity: “Microsoft Corp. has canceled some leases for US data center capacity, according to TD Cowen, raising broader concerns over whether it’s securing more AI computing capacity than it needs in the long term.” Now both small caps and the Magnificent 7 are underperforming the broader market.

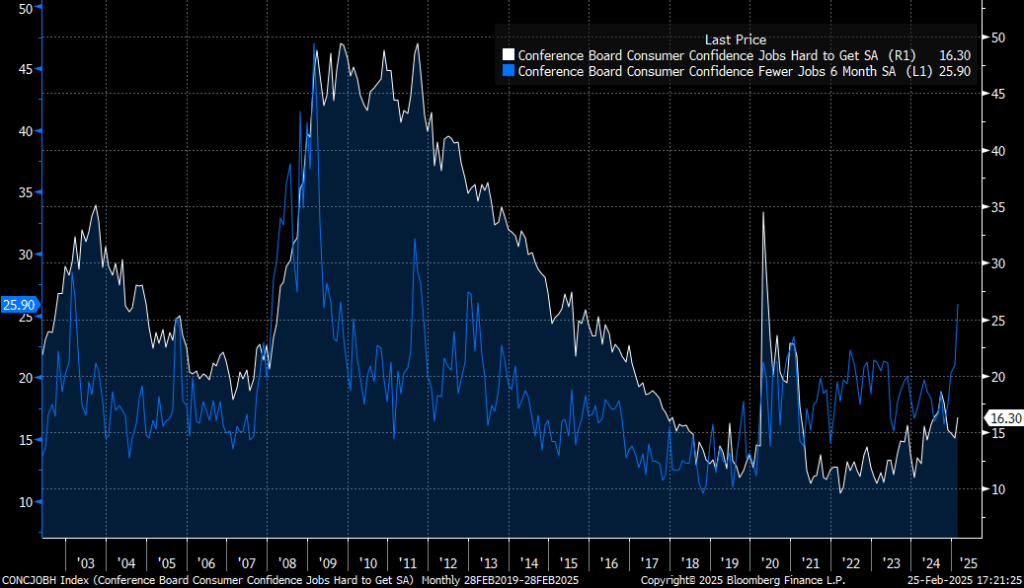

Consumer is showing more weakness signs. Weak retail sales were accompanied by poor Walmart guidance. Conference board consumer confidence is flashing red unemployment signs.

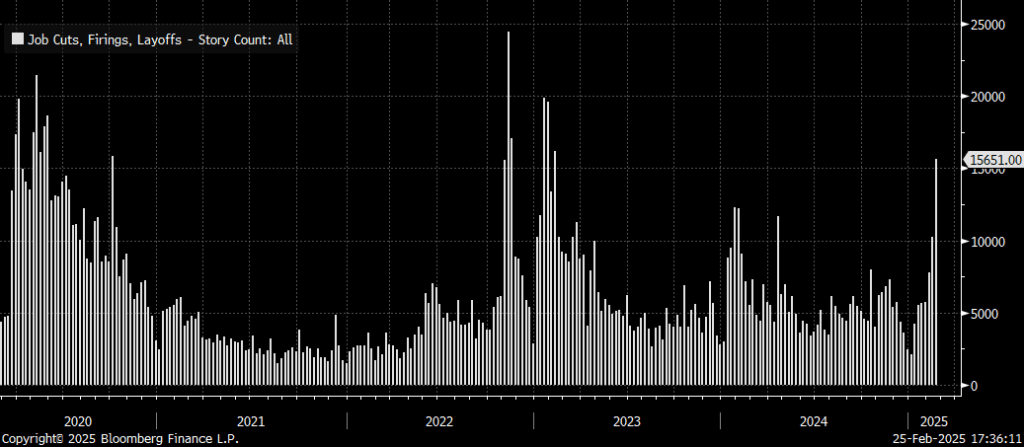

Number of “layoffs” mentions in the news articles is spiking again.

Bottom line: economy is weakening, unemployment can start rising again, bonds remain more attractive than stocks.

Leave a comment