Trump trade so far is diverging from 2016 analogy. At the moment most markets see much smaller incremental policy change compared to 2016. On top of that, rates stay restrictive enough to slow the economy further: demand, employment, margins, inflation – are all softening.

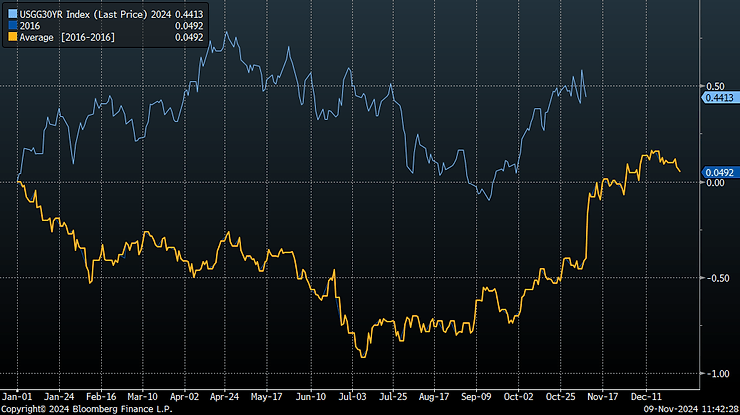

Bonds aren’t selling off post elections, despite large intraday volatility on the election date. 30-year yields are basically flat in the last 2 weeks.

Dollar strengthens less than in 2016 too (percent change ytd).

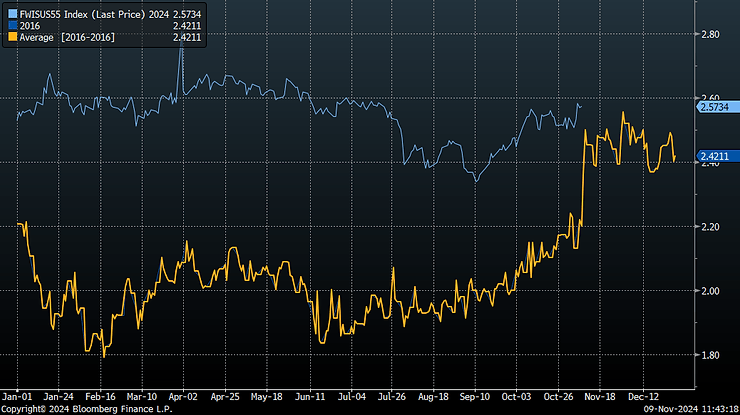

So are inflation swaps (actual value).

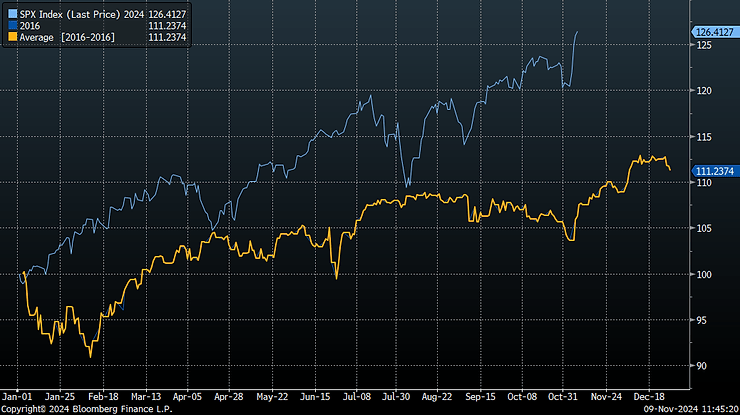

Equities are a major difference, particularly small caps.

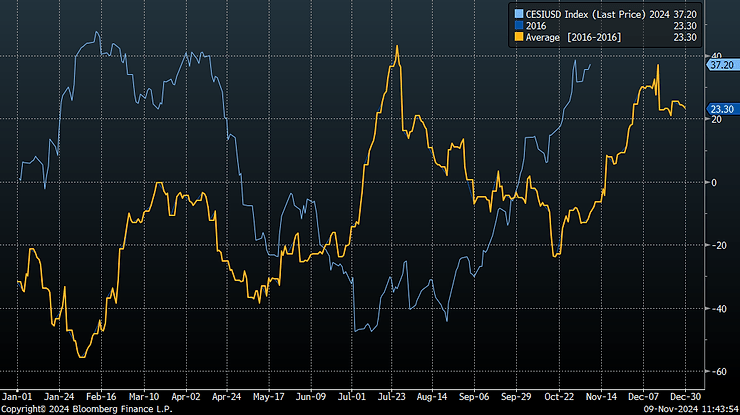

Meanwhile US eco surprise index advanced much sooner before the election date this time. And it was an important driver of yields and equities before the election. A lot of market moves and actual physical pre-ordering happened in anticipation of Trump’s arrival. And it certainly can continue for a while before tariffs are implemented or policy becomes clearer.

But underneath economic growth stays weakish. Analysts are revising earnings lower, leading indices are deteriorating, as capex cycle is expected to weaken further.

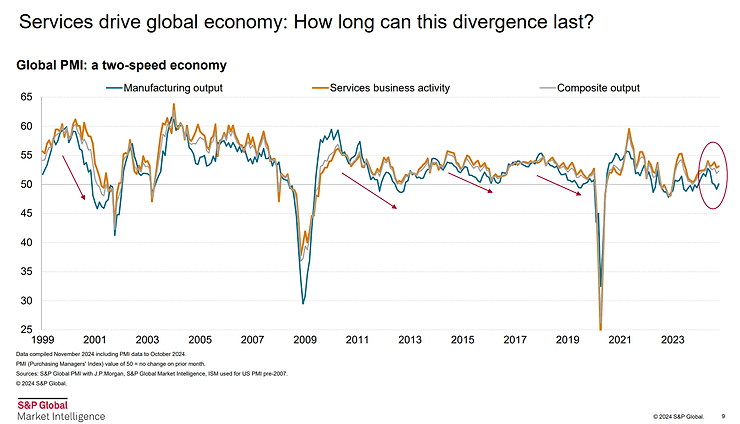

Services are keeping overall activity on a healthy level. However, they usually lag manufacturing for 6-9 months, until financial conditions start worsening (stocks decline). And the risk of spill over is rising.

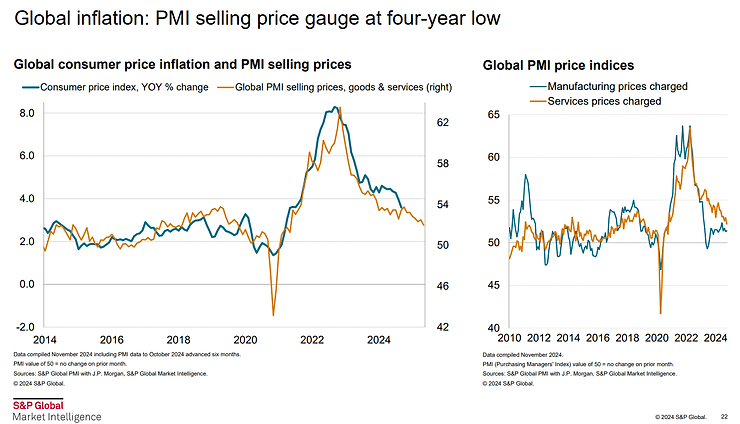

Services pricing power is diminishing, pointing to lower global core CPI going forward.

US corporate margins are slowly deteriorating on a trailing 12 months basis. Last time Trump was elected, US was exiting its mini industrial/shale recession thanks to reacceleration of oil and gas output and related industrial capex. This time the cycle is rolling over instead.

US corporates are also more pronounced about that in their earning calls as well. Diffusion of “strong-less-weak” demand is deteriorating.

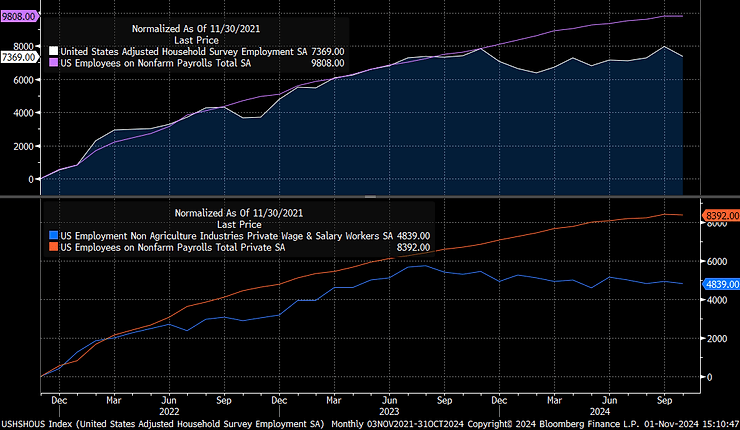

US employment is weakening further after a spike in September. Despite weather and strikes or other one-offs, flows of people not in labor force into employment are declining – hiring remains weak.

NFP and household surveys continue to diverge: absolute number of jobs added in the last 3 years – total and private-only differs by 2.5-3.5 million. Household survey includes workers not at work due to weather in total employment, so is not affected by the hurricanes this time.

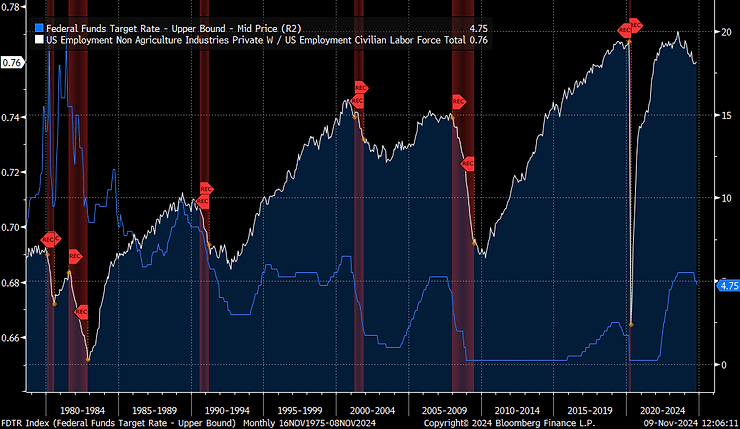

Employment is also deteriorating at current level of interest rates: private employment to labor force ratio peaked in June 2023. Current decline is consistent with falls that happened during previous recessions.

Small businesses sales and prices sentiment, parts of NFIB survey, are pointing to weakening nominal GDP going forward. IMO, bonds remains attractive, unless another trillion stimulus is announced, and equities are too risky

Leave a comment